What Foreclosure Really Means

Foreclosure is the legal process a lender uses to take back a home after the borrower stops making mortgage payments. That is it in plain English.

When someone searches for what a foreclosure is, they are usually not doing it out of curiosity. They are either behind on payments, worried they might fall behind, or trying to understand if buying one is a smart move.

There is emotional weight on both sides.

For homeowners, foreclosure can feel like failure, panic, or embarrassment. It often comes after job loss, rising insurance costs, medical debt, or simply underestimating how expensive homeownership really is. I have seen people stretch to buy a house, only to get blindsided later by taxes, repairs, or rising payments.

For buyers and investors, foreclosure sounds like an opportunity. Discount. Equity. Deal. But that word also carries risk, legal complexity, and hidden costs that most beginners do not fully understand.

That is why understanding foreclosure matters.

If you are a homeowner, you need to know what stage you are actually in and what options still exist. If you are a buyer, you need to know what you are stepping into before you wire earnest money or show up to an auction.

In this guide, I am going to break down:

- What foreclosure actually means

- The exact stages from missed payment to auction

- The terminology that confuses most people

- The real risks no one talks about

- And how all of this impacts buyers and investors

If you are trying to understand the bigger picture of how foreclosure properties fit into the real estate investing process, see our complete guide to Buying Foreclosed Homes: Start to Finish Guide.

Let’s start by clearing up the confusion around how foreclosure actually begins.

What Is Foreclosure?

Foreclosure is not random. It is a structured legal process triggered by missed mortgage payments.

At its core, foreclosure exists because a mortgage is a secured loan. The property itself is the collateral. If the borrower stops paying, the lender has the legal right to recover the asset tied to the debt.

Let’s break that down simply.

Simple Definition

Foreclosure is the legal process where a lender takes back a property after the borrower fails to make agreed upon mortgage payments.

When you buy a home with a mortgage, you do not technically own it free and clear. The bank has a lien against the property. That lien secures their money.

If payments stop long enough, the lender does not just shrug and move on. They initiate a legal process to seize and sell the property to recover the remaining loan balance.

Banks do not foreclose because they want houses.

They foreclose because they want their capital back.

From a risk management perspective, a non paying loan is a liability on their balance sheet. Foreclosure allows them to convert that non performing loan back into cash through an auction or resale.

It is not emotional for them. It is math.

Why Foreclosure Happens

Foreclosure rarely starts with one missed payment. It usually builds from financial pressure that compounds over time.

The most common trigger is job loss. One disrupted income stream can unravel a household budget quickly, especially if there is no emergency fund.

Adjustable rate mortgage resets can also shock homeowners. A payment that was manageable at a lower rate can suddenly jump hundreds of dollars per month.

Medical debt is another big one. Unexpected hospital bills can derail even financially responsible households.

Overleveraging plays a role too. Some buyers stretch their budget to win bidding wars or assume appreciation will bail them out. When expenses rise or income drops, there is no margin for error.

Property value declines can make things worse. If a homeowner owes more than the property is worth, selling becomes difficult without bringing cash to closing.

Most foreclosures are not caused by one bad decision. They are caused by thin financial margins meeting unexpected pressure.

And here is something important to understand.

Foreclosure does not happen overnight.

It unfolds in stages.

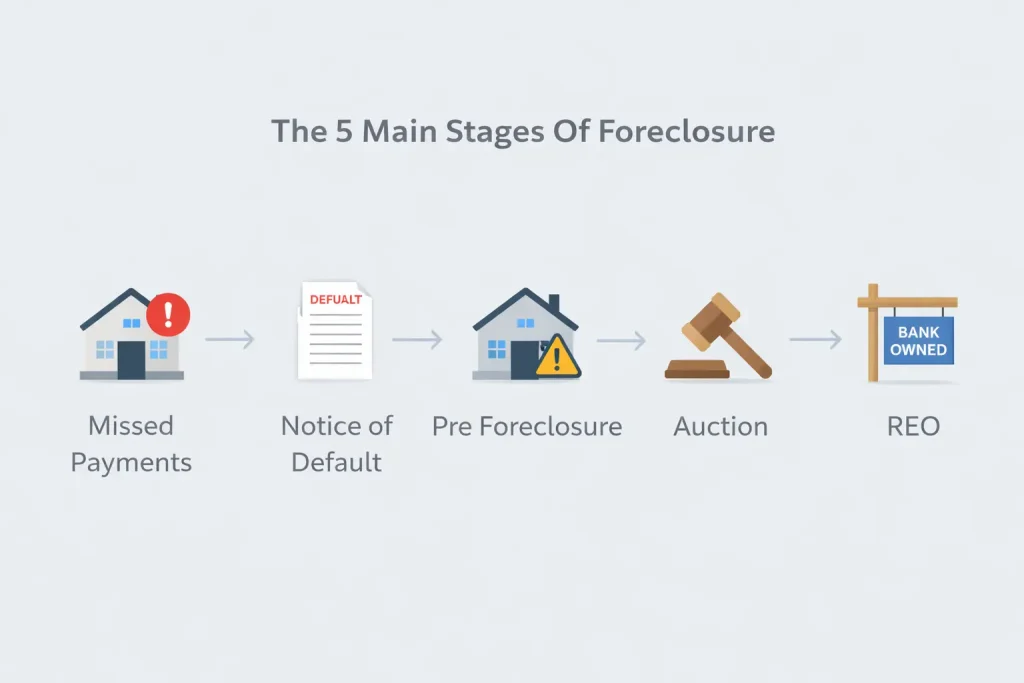

The 5 Main Stages Of Foreclosure

Foreclosure is a process, not an event. If you understand the stages, you stop guessing and you start making better decisions, whether you are the homeowner trying to prevent it or the buyer trying to evaluate it.

The exact timeline varies by state, but the structure is usually the same.

Here are the five main stages.

1. Missed Payments

Foreclosure starts with missed payments, but it usually takes time before the legal machinery kicks in.

At 30 days late, you are typically marked delinquent. Fees begin. Your lender is now tracking you as a risk.

At 60 days late, the situation gets more serious. The lender will usually escalate contact attempts. Phone calls. Letters. Emails. Sometimes all three.

At 90 plus days late, you are generally considered in default. This is where many lenders begin preparing the foreclosure file, even if they have not officially filed anything yet.

During this stage, the lender is not trying to be your friend. They are trying to either get you paying again or set up the next step.

The takeaway is simple. The earlier you act, the more options you have.

2. Notice Of Default (Pre Foreclosure Begins)

This is the point where foreclosure becomes real on paper.

A Notice of Default is a formal legal filing that states the borrower is in default and the lender is beginning the foreclosure process. In many states it becomes a public record, meaning anyone searching public notices can see it.

Here is what most people get wrong.

Even after the Notice of Default is filed, the borrower still owns the home. The property has not been taken back yet. It has not been auctioned yet. It is not bank-owned yet.

It is in limbo.

At this stage, many homeowners ask, What Does Pre Foreclosure Mean For Homeowners? because the property has not yet been repossessed.

The implication here is that there is still time, but the clock is now ticking.

3. Pre Foreclosure Options

Pre foreclosure is the window where homeowners can still stop the process, but it requires action and usually requires money, paperwork, or both.

One option is reinstatement, which means catching up on the missed payments plus fees. If you can do that, you may be able to bring the loan current and end the foreclosure track.

Another option is loan modification. This is where the lender agrees to adjust the loan terms to create a more affordable payment. Not everyone qualifies, but it is a real path for some homeowners.

Refinancing can work in certain situations, but it depends on credit, income, and whether the home still appraises. If the homeowner is already behind, refinancing is usually harder than people think.

Selling before auction is often the cleanest solution. It stops the foreclosure, protects credit more than a completed foreclosure, and gets the homeowner out without the court hammer dropping.

If the homeowner owes more than the home is worth, then a short sale may come into the conversation. Some distressed owners attempt a negotiated sale instead of foreclosure, which is where understanding Short Sale Vs Pre Foreclosure: Key Differences becomes important.

The takeaway is that pre foreclosure is not the end. It is the decision point.

4. Foreclosure Auction’

If the foreclosure is not stopped, the next stage is the foreclosure auction.

This is typically a public auction held at a courthouse or conducted online depending on the county and state. The home is sold to the highest bidder, usually with strict terms and very little room for error.

Most auctions require cash or certified funds, and the buyer often has to bring a significant deposit immediately. Traditional financing usually does not work here because the closing window is short and the property is sold as is.

There are also title risks. You may inherit liens or legal issues depending on how the auction is structured and what was not cleared prior to sale.

Inspections are limited or nonexistent. In many cases, you are buying based on exterior view, public data, and your ability to price risk correctly.

This is why auctions can create deals, but they can also create disasters.

Not every property sells at auction. Many revert to the lender.

5. REO (Real Estate Owned)

REO stands for Real Estate Owned. This is what happens when a property does not sell at auction and the lender ends up taking it back.

At that point, the bank becomes the owner, and the property usually gets listed for sale through a real estate agent. These homes are still sold as is most of the time, but the buying process looks more like a normal transaction than an auction does.

When a home fails to sell at auction, it becomes bank owned property, also called REO. To understand this stage in detail, read What Is Reo Foreclosure And How Does It Work?

Buyers often confuse terminology here, so it helps to know the exact Reo Foreclosure Meaning And How It Affects Buyers.

In today’s market conditions, understanding Reo Properties Meaning In Today’s Real Estate Market can help investors spot opportunities others miss.

The big implication is this. REO is usually the most accessible stage for everyday buyers, but it still comes with foreclosure level risk if you do not do your homework.

Key Foreclosure Terms Every Buyer Should Know

If you do not understand the terminology, you will misjudge the risk. Foreclosure language sounds intimidating, but once you define the terms clearly, it becomes manageable.

Here are the core terms every buyer and investor should know.

Notice of Default

A Notice of Default is the formal document filed by a lender stating the borrower is behind on payments and the foreclosure process has begun. It is often recorded publicly.

This does not mean the home is owned by the bank yet. It means the legal clock has started.

Lis Pendens

Lis Pendens is Latin for pending lawsuit. It is a public notice that a property is involved in a legal action, often foreclosure.

For buyers, this signals that the property’s title may be tied up in court proceedings. It is not automatically a deal breaker, but it does require caution and proper title research.

Trustee Sale

A Trustee Sale is the actual foreclosure auction in states that use a deed of trust instead of a traditional mortgage structure.

This is where the property is sold to the highest bidder. Terms are strict. Timelines are short. Financing options are limited.

If you are attending a trustee sale, you should already know your numbers before you show up.

Deficiency Judgment

A Deficiency Judgment happens when the home sells for less than what is owed on the mortgage, and the lender pursues the borrower for the remaining balance.

This affects sellers more than buyers, but it is important context when negotiating with distressed homeowners.

In some states, deficiency judgments are limited or prohibited. In others, they are fully enforceable.

Redemption Period

A Redemption Period is a window of time after the foreclosure sale during which the original homeowner may have the right to reclaim the property by paying the full debt plus costs.

Not all states have redemption periods, but where they exist, they can create uncertainty for buyers who assume ownership is final immediately after auction.

Understanding your local state laws here is critical.

REO

REO stands for Real Estate Owned. This refers to a property that has gone through auction and failed to sell, resulting in the lender taking ownership.

At this stage, the property is usually listed on the retail market through an agent. The process feels more traditional, but the property is still typically sold as is.

Short Sale

A Short Sale occurs when a lender agrees to let a homeowner sell the property for less than the remaining loan balance to avoid foreclosure.

Unlike a foreclosure, the homeowner still owns the property and is voluntarily negotiating with the bank. The process can take months and requires lender approval before closing.

Many new investors confuse distressed sale types, which is why reviewing Short Sale Vs Foreclosure: What Buyers Must Know can prevent costly mistakes.

The bottom line is this. If you understand the language, you can evaluate the opportunity with clear eyes instead of guesswork.

Are Foreclosures Actually Cheaper?

Sometimes. Not always.

That is the honest answer.

Foreclosures have the potential to sell below market value, but assuming every foreclosure is a deal is how beginners get burned.

Let’s break down what actually determines the price.

First, there is discount potential. Banks are not emotionally attached to properties. They want to move non performing assets off their books. In certain cases, especially if the home needs work or has been sitting, they may price aggressively to move it.

That creates opportunity.

But opportunity does not mean automatic profit.

Condition issues are the biggest variable. Many foreclosed homes have deferred maintenance. Some have been vacant for months. Others were neglected long before the foreclosure started.

Roof problems. HVAC failures. Plumbing leaks. Mold. Vandalism.

The photos rarely tell the full story.

Repair uncertainty is what separates experienced investors from hopeful buyers. A property that looks like it needs twenty thousand in work can quickly turn into forty thousand once you open walls or inspect major systems.

If you underestimate repairs, the discount disappears fast.

Competitive bidding is another factor most people overlook. Auctions can get heated. Retail REO listings can attract multiple offers. Investors show up with cash and clear timelines.

In strong markets, foreclosures can sell at or even above market value because buyers are chasing limited inventory.

Institutional investor activity also matters. In certain areas, large investment firms and hedge funds buy distressed properties in bulk. That competition pushes prices up and margins down.

The takeaway is simple.

While foreclosures can sometimes sell below market value, it is not guaranteed. Which is why we break down the full analysis in Are Foreclosure Homes Cheaper Than Traditional Homes?

A foreclosure can be a deal.

But only if the numbers still make sense after you account for reality.

Pros And Cons Of Buying A Foreclosed Home

Buying a foreclosed home can create opportunity, but it also concentrates risk. The key is understanding both sides before you wire money or submit an offer.

Here is the reality in simple terms.

Pros

Potential equity

The biggest upside is built in equity. If the property is priced below comparable sales and the repair costs are controlled, you may walk into instant value.

That is the appeal.

You are not paying retail for granite countertops and staging. You are buying distress and solving it.

Less emotional sellers

When negotiating with a bank, you are not dealing with a family who painted the nursery or planted the backyard trees.

You are dealing with an asset manager.

That removes emotional pricing. The conversation becomes numbers and timelines instead of feelings.

Bank pricing models

Banks use data driven models to price properties. They look at comparable sales, days on market, and absorption rates.

Sometimes this works in your favor. Especially if they price to move inventory quickly instead of squeezing every dollar out of the sale.

That is where disciplined buyers can create margin.

Cons

Condition risk

Most foreclosures are sold as is. No repairs. No credits. No promises.

If the HVAC dies two weeks after closing, that is on you.

Deferred maintenance is common, and major capital expenses can wipe out projected profit fast.

Title issues

Not every foreclosure is clean. There can be liens, unpaid taxes, or legal complications that need to be resolved.

A proper title search is not optional. It is mandatory.

No disclosures

Traditional sellers usually provide property disclosures. Banks often provide minimal information because they have never lived in the property.

You are operating with limited historical knowledge.

That increases uncertainty.

Auction risk

If you are buying at auction, risk goes up even more. Limited inspection access. Strict deposit requirements. Short closing windows.

One miscalculation can get expensive quickly.

Before making an offer, review the complete breakdown in Pros And Cons Of Buying A Foreclosed Home Explained.

The goal is not to avoid risk.

The goal is to price it correctly before you commit.

Risks Of Buying Foreclosure Properties

Foreclosures are not dangerous because they are foreclosures. They are dangerous when buyers assume they are automatic deals.

Risk shows up in three main buckets. Financial, legal, and market.

If you understand these clearly, you reduce surprises.

Financial Risks

The biggest financial mistake I see is underestimated rehab.

You walk through a property and think it needs cosmetic updates. Paint. Flooring. Maybe a kitchen refresh.

Then the inspector finds foundation movement. Or the sewer line is cracked. Or the roof has two years left.

Budgets inflate fast. Especially on older homes.

ARV miscalculation is another common issue. ARV means After Repair Value. It is what the property should sell for once renovated.

If you overestimate ARV by even five percent, your margin can disappear. Markets shift. Buyer demand cools. Comparable sales change.

Holding costs are the silent killer. Taxes. Insurance. Utilities. Interest payments. Lawn maintenance.

Every extra month you hold the property chips away at profit. Time is not neutral. It costs money.

The implication here is simple. If your numbers only work in a perfect scenario, the deal is too tight.

Legal Risks

Legal issues can delay or destroy a deal if you are not careful.

Liens are common. Unpaid contractor bills. Tax liens. Utility balances. If they are not cleared properly, they can follow the property.

HOA claims are another surprise. Some associations have unpaid dues that attach to the home.

Redemption rights add complexity in certain states. In those cases, a former owner may legally have a period after auction to reclaim the property by paying off the debt.

If you do not understand your state laws, you are guessing.

A thorough title search and working with a competent closing attorney is not optional here.

Market Risks

Market risk is what most beginners ignore.

Overpaying at auction happens more often than people admit. Bidding becomes competitive. Ego gets involved. Numbers get stretched.

Institutional competition also matters. Large investors and hedge funds buy in bulk in certain markets. They operate on thinner margins because of scale.

That pushes smaller investors into tighter deals.

The reality is this. Not every foreclosure is a hidden gem. Some are simply properties that need more work than they are worth.

If you are actively searching for opportunities, choosing the Best Foreclosure Website For Finding Real Deals can dramatically impact deal quality.

Better data leads to better decisions.

And better decisions are what separate long term investors from one deal wonders.

Who Should And Should Not Buy Foreclosures?

Foreclosures are not for everyone. They reward preparation and punish thin margins.

Before you chase a deal, you need to ask whether your situation actually fits this type of property.

Let’s break it down honestly.

A Good Fit For Foreclosures

Investors with cash reserves are usually in the strongest position.

If you have liquidity, you can move fast, handle unexpected repairs, and survive delays. Cash gives you flexibility at auction and leverage when negotiating with banks.

Experienced flippers also tend to navigate foreclosures better.

They understand ARV. They price renovation risk correctly. They already have contractors, systems, and a buffer built into their numbers.

Buyers comfortable with risk can also make it work.

This does not mean reckless. It means realistic. You understand that timelines can shift. Repairs can expand. Title work can take time.

You are not relying on everything going perfectly.

Not Ideal For Foreclosures

First time buyers with minimal cash should be careful.

If you are stretching to make the down payment and have no reserve fund, a surprise roof replacement can turn excitement into panic quickly.

Buyers needing move in ready homes are usually better off with traditional listings.

Most foreclosures require at least some level of repair, even if it is minor. If you need something turnkey with no disruption, foreclosure inventory rarely fits that requirement.

Buyers relying on strict financing timelines may also struggle.

Auction purchases often require quick closings. Some properties will not qualify for traditional loans due to condition issues. Appraisals can come in low. Lenders can delay.

If your financing is tight and your approval window is narrow, you are operating with little room for error.

The takeaway is simple.

Foreclosures are tools. In the right hands, they create opportunity. In the wrong situation, they amplify risk.

The question is not whether foreclosures are good or bad.

The question is whether they fit your financial position and risk tolerance right now.

Understanding Foreclosure Before Taking Action

Foreclosure is not something to fear. It is something to understand.

Knowledge reduces risk.

When you know the stages, the terminology, and the legal structure behind foreclosure, you stop reacting emotionally. You start evaluating logically.

Not all distressed properties are equal.

A pre foreclosure is not the same as an auction. An auction is not the same as an REO. A short sale is not the same as a completed foreclosure. Each comes with different timelines, leverage points, and risks.

If you lump them together, you will price them wrong.

Terminology clarity matters more than most people realize. The difference between a Notice of Default and a trustee sale can mean months of timing difference. The difference between a redemption state and a non redemption state can change your ownership security.

Process awareness prevents costly mistakes.

The people who get burned are usually not reckless. They are uninformed. They skip due diligence. They assume the discount is automatic. They underestimate rehab or overestimate value.

Understanding foreclosure does not guarantee profit.

But it dramatically lowers the probability of disaster.

If you are ready to move beyond definitions and actually learn how to find, evaluate, and purchase foreclosure deals step by step, start with our full guide on Buying Foreclosed Homes: Start to Finish Guide.