Most Foreclosure Deals Are Not Real Deals

If you are searching for the best foreclosure website, you are probably trying to find a deal.

But before you even start comparing platforms, it helps to understand how the foreclosure process actually works. If you need a full breakdown of the legal timeline, auction stages, and risk factors, I covered that in detail inside my guide on foreclosure stages, terms, and risks.

Because here is the uncomfortable truth.

Just because a property says foreclosure does not mean it is discounted.

I have seen countless buyers assume that the word foreclosure automatically equals equity. It does not. Sometimes it just equals complexity.

A lot of these listings fall into one of a few categories.

Already under contract and never updated.

Priced right at market value because the bank knows what it has.

Require full cash with a two week closing window.

Still occupied, which means you are inheriting a situation, not just a property.

That is where a lot of first time buyers get burned.

They see the word foreclosure and think they found a shortcut around high prices, high rates, and bidding wars. But what they really found was a listing that looks discounted on the surface and behaves like a normal retail deal underneath.

The goal is not to find a foreclosure.

The goal is to find a real deal.

So what is actually the best foreclosure website for finding real deals?

What People Are Really Looking For When They Google Best Foreclosure Website

When someone searches best foreclosure website, they are not looking for a pretty interface.

They are looking for leverage.

Most buyers do not even realize what they are actually searching for. They think they want a list of homes. What they really want is access before everyone else.

Here is what that usually translates to.

Updated Inventory

If the data is stale, the deal is gone.

One of the biggest frustrations I see is buyers chasing properties that are already under contract or already sold. Nothing wastes more time than analyzing a deal that no longer exists.

Updated inventory is not a luxury. It is the baseline.

If the platform is not syncing regularly, you are playing catch up in a market that already moves fast.

Pre Foreclosures Before They Hit Auction

This is where things get interesting.

Pre foreclosures are properties where the homeowner is behind but the bank has not taken full control yet. That window creates opportunity.

Less competition.

More negotiation flexibility.

More time to structure a deal.

By the time a property hits auction, the feeding frenzy has already started. Pre foreclosure data is what gives you breathing room.

Bank Owned Properties Or REOs

When a foreclosure goes back to the lender, it becomes a bank owned property.

These are often listed more traditionally, sometimes even on the MLS. The key difference is the seller.

You are negotiating with an institution, not an emotional homeowner.

That changes everything.

Banks care about net proceeds and timelines. If you understand that, you can structure stronger offers.

Transparent Auction Terms

A lot of people jump into foreclosure auctions without reading the fine print.

Buyer premiums.

Non refundable deposits.

Short closing windows.

As is condition with limited inspection access.

If the website does not clearly outline auction terms, you are stepping into risk blindly.

Clarity matters more than hype.

Financing Eligibility

This one gets ignored constantly.

Some foreclosures qualify for traditional financing. Some do not.

If the property has major condition issues, most lenders will not touch it. That means cash or hard money only.

And in today’s rate environment, where cash flow is already tight, financing structure can make or break the deal. Analysis of Problems by rRealEs…

Before you fall in love with a listing, you need to know how it can actually be purchased.

Local Filtering

National databases are great.

But real estate is local.

You need to filter by city, county, and sometimes even neighborhood level trends. Taxes, insurance, rental demand, and local regulations vary wildly by area.

If you cannot narrow your search properly, you will spend hours analyzing properties that do not even fit your strategy.

The website does not create the deal.

The data and access do.

If the platform gives you earlier data, clearer terms, and better filtering, you gain an edge.

And in this market, an edge is everything.

The 4 Best Foreclosure Websites Ranked By Strategy

There is no single best foreclosure website for everyone.

The right platform depends on your strategy, your capital, and your risk tolerance.

Some sites are research engines.

Some are auction platforms.

Some are institutional pipelines.

If you understand what each one is built for, you stop browsing and start targeting.

Let’s break them down.

Foreclosure.com

Best For Research And Pre Foreclosures

If you want the widest net possible, this is usually where you start.

Foreclosure.com stands out because it aggregates massive amounts of foreclosure related data into one place. That includes pre foreclosures, bank owned properties, government listings, and auction properties.

The pre foreclosure access is the real advantage here.

You are seeing properties before they hit the auction stage, which means less competition and more room to negotiate.

Why it stands out:

Largest aggregated foreclosure database

Pre foreclosures which give earlier access

REO and government listings

Strong national coverage

Pros:

- Broad data coverage across multiple foreclosure stages

- Early stage opportunities before public auction

- Subscription model filters out casual browsers

Cons:

- You must verify data independently

- Some listings can be stale

- Requires effort and due diligence

This is not a magic button. It is a data tool.

Who it is best for:

Investors hunting early stage opportunities

Buyers willing to dig and cross reference

Anyone who wants wide inventory fast

This is typically where I would begin research before narrowing down into more specific platforms.

Hubzu

Best For Online Bank Auctions

Hubzu is built around online auctions for bank owned properties.

If you do not want to stand on courthouse steps, this platform offers a cleaner experience. The bidding process is visible and structured.

You can see competing offers and timelines directly on the listing page.

Why it stands out:

Transparent bidding interface

Primarily bank owned inventory

Some properties qualify for financing

Pros:

- Cleaner process than courthouse auctions

- Clear visibility into active bids

- Centralized online format

Cons:

- Buyer premiums on many properties

- Competitive bidding environment

- Reserve prices that may not be obvious upfront

Hubzu is not passive investing. You need to move quickly and run your numbers tightly.

Best for:

Intermediate buyers

Investors comfortable operating in auction environments

If you understand margins and do not overbid emotionally, this platform can work.

Xome

Best For Bank Controlled Inventory

Xome sits somewhere between traditional listings and auctions.

They have direct lender relationships, which means a consistent flow of bank controlled properties. Some are auction based. Some are sold more traditionally.

That hybrid model gives flexibility.

Why it stands out:

Direct ties to large lenders

Mix of auction and traditional REO sales

Variety in property condition

Pros:

- Strong institutional inventory pipeline

- Decent filtering tools

- Access to both auction and non auction deals

Cons:

- Buyer premiums in auction scenarios

- Often sold as is

- Fast closing timelines

Best for:

Cash ready investors

Buyers with renovation experience

If you do not have reserves for unexpected repairs, this is not the place to experiment.

Auction.com

Best For Experienced Investors

Auction.com is volume.

This platform operates at an institutional level with thousands of properties across the country. You will find both online auctions and courthouse events listed here.

The upside is scale. The downside is competition.

Why it stands out:

Massive nationwide inventory

High institutional deal flow

Combination of courthouse and online auctions

Pros:

- Real potential for discounted purchases

- High deal volume

- Established national presence

Cons:

- Heavy cash requirements

- Occupancy risk on many properties

- Limited inspection access

- Extremely competitive

This is where serious investors play.

Best for:

Experienced investors only

If you do not understand title risk, repair budgeting, and holding costs, this platform can expose you quickly.

Each of these platforms serves a different purpose.

The key is matching the platform to your strategy instead of assuming one site solves everything.

Which Website Is Actually Best

The honest answer is this.

There is no universally best foreclosure website.

There is only the platform that fits your strategy.

If you are chasing the wrong type of deal for your experience level or capital stack, the website does not matter. You will force something that does not fit.

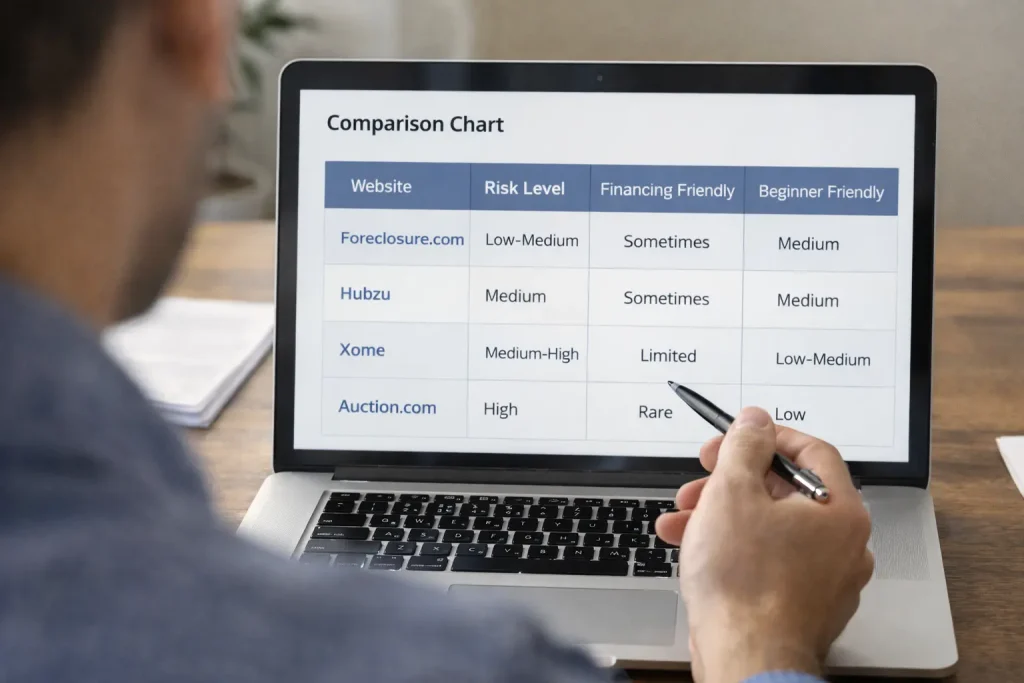

Here is a simple breakdown to make this clearer.

| Website | Best For | Risk Level | Financing Friendly | Beginner Friendly |

|---|---|---|---|---|

| Foreclosure.com | Research and early deals | Low to Medium | Sometimes | Medium |

| Hubzu | Online auctions | Medium | Sometimes | Medium |

| Xome | Bank REO auctions | Medium to High | Limited | Low to Medium |

| Auction.com | Serious investors | High | Rare | Low |

Now let’s interpret that table instead of just staring at it.

Foreclosure.com is more of a research engine. It gives you earlier stage data, especially pre foreclosures. The risk tends to be lower because you still have room to negotiate before auction chaos begins.

Hubzu is auction focused, but in a more structured online environment. The risk increases because you are bidding against others and often paying premiums.

Xome leans further into bank controlled inventory with faster timelines and heavier as is exposure. If your numbers are loose, it will show quickly.

Auction.com is volume and velocity. High competition. High risk. Potentially high reward. Not forgiving.

The best foreclosure website depends entirely on your strategy.

🧮 Want early data and negotiation flexibility? → Foreclosure.com

🏠 Want cleaner online auctions without courthouse drama? → Hubzu

💰 Want institutional inventory directly from lenders? → Xome

🔥 Want maximum upside with maximum risk? → Auction.com

Match the platform to your experience level.

That alone will eliminate half the mistakes most people make.

How To Actually Find A Real Deal

Most blogs stop at listing websites.

That is not where the money is made.

A real foreclosure deal is not defined by the word foreclosure. It is defined by math.

Here is the formula I use.

Market Value minus Repairs minus Risk Premium minus Holding Costs equals Margin.

If there is no margin left, it is not a deal.

It is just a discounted headline.

Let’s break this down properly.

ARV Analysis

Everything starts with value.

ARV stands for After Repair Value. It is what the property should realistically sell for once it is renovated to match comparable homes in the area.

You cannot guess this.

You need recent sold comparables that match square footage, bed and bath count, lot size, and condition. Not active listings. Sold data.

If renovated homes are selling for 400k, that is your ceiling.

And here is the part nobody talks about.

Lenders quietly cap you based on that value. If the appraisal comes in low, your deal falls apart or you bring cash to closing.

If your ARV is inflated, your entire deal collapses.

Repair Budget Buffers

This is where beginners underestimate everything.

If your contractor says 40k in repairs, assume it is at least 46k to 50k.

Add a 15 to 20 percent buffer.

Foreclosures and distressed homes often hide issues behind walls. Old plumbing. Roof problems. Electrical panels that need updating.

Once you open things up, surprises show up.

Underestimating rehab costs is one of the fastest ways to erase profit.

Build the buffer in from the beginning.

Title And Lien Checks

You are not just buying a house.

You are buying its legal history.

Unpaid taxes. Mechanics liens. HOA dues. Judgment liens. These can attach to the property.

A proper title search is non negotiable.

If you skip this step or assume the platform handled it for you, you are gambling.

Always confirm clean title before closing. If there are liens, factor them into your numbers or walk away.

Occupancy Status

Vacant and occupied are two very different investments.

If the property is occupied, you may be inheriting a tenant or a former owner who refuses to leave.

Evictions can take months in some states. That means carrying costs with zero income.

You need to know:

Is it vacant

Is it tenant occupied

Is it owner occupied

Each scenario changes your risk profile.

Financing Constraints

Some foreclosures qualify for traditional financing.

Many do not.

If the property has major condition issues, lenders may reject it outright. That forces you into cash or hard money territory.

Higher interest. Shorter timelines. Higher monthly carrying costs.

And in a market where interest rates are already elevated and cash flow margins are thin, financing structure can make or break the deal.

Before you submit an offer, confirm how it will be financed.

Not how you hope it will be financed.

Here is the takeaway.

If the numbers do not work after you account for value, repairs, risk, holding costs, title, occupancy, and financing, it is not a real deal.

It is just a foreclosure.

And those are not the same thing.

Common Foreclosure Mistakes

Most foreclosure losses are self inflicted.

It is rarely the website that causes the damage. It is the assumptions buyers bring into the deal.

And when margins are already tight and money feels stretched, small mistakes turn into big financial stress fast.

Let’s walk through the ones I see over and over.

Assuming Foreclosure Equals Discount

This is the biggest trap.

Just because a property is labeled foreclosure does not mean it is priced below market.

Banks know how to price assets. Auction platforms know how to create bidding pressure. Sometimes the “deal” is priced right where retail comps are.

If you are already struggling with affordability or trying to stretch into ownership, overpaying for a foreclosure can put you in a worse position than buying a traditional listing.

A foreclosure should be discounted because of risk.

If there is no discount, you are just absorbing risk for free.

Ignoring Buyer Premiums

Auction sites often charge buyer premiums.

Five percent. Ten percent. Sometimes more.

That gets added on top of your winning bid.

So if you win at 300k with a ten percent premium, you are really paying 330k before you even factor in closing costs or repairs.

For buyers already stressed about cash reserves or down payments, this can blow up your numbers quickly.

You have to account for the full acquisition cost, not just the bid price.

Not Checking Comparable Sales

Active listings do not determine value.

Sold listings do.

I have seen buyers justify a purchase because “another house is listed for 420k.” That means nothing.

What did similar homes actually close at in the last 60 to 90 days?

If you skip comp analysis, you are speculating.

And speculation is dangerous when rates are high and every extra dollar increases your monthly payment pressure.

Underestimating Rehab

This one quietly destroys profit.

Older homes often hide expensive problems. Roof issues. Sewer lines. Electrical panels. Foundation cracks.

If you budget 30k and the real number ends up at 50k, that gap comes out of your reserves.

And if you do not have reserves, it comes out of credit cards or personal loans.

That is how a “deal” turns into long term debt stress.

Add buffers. Build in contingencies. Assume something will go wrong.

Because something usually does.

Forgetting Holding Costs

Every month you own the property, you are paying something.

Mortgage or hard money interest.

Taxes.

Insurance.

Utilities.

Maintenance.

Even if you are flipping, time is money.

If the property takes longer to sell or rent than expected, those carrying costs eat into margin fast.

And in a market where insurance premiums and property taxes have been rising sharply in many areas, ignoring holding costs is not a small oversight.

Here is the bigger theme.

A lot of people searching for the best foreclosure website are already feeling financial pressure. Rising costs. Tight budgets. Anxiety about making the wrong move.

The last thing you want to do is compound that stress with a poorly analyzed foreclosure.

Foreclosures can create opportunity.

But only if you remove the emotion and respect the math.

Final Verdict

The best foreclosure website is not the one with the flashiest interface.

It is the one that gives you access before everyone else.

Speed matters.

Data matters.

Timing matters.

If you are seeing the deal at the same time as every other investor in your market, you are not early. You are late.

That is why I view these platforms differently.

Foreclosure.com is not an auction arena. It is a research engine.

It is the broadest starting point.

It aggregates pre foreclosures, REOs, and government listings into one searchable layer. That matters because early data creates optionality.

Optionality creates leverage.

From there, you narrow down.

You validate comps.

You estimate repairs.

You check title exposure.

You confirm financing.

Then, if the property moves toward auction or transitions into bank owned inventory, you cross check it against platforms like Hubzu, Xome, or Auction.com.

That layered approach keeps you from relying on a single source.

I personally start there.

Then I cross check with auction platforms.

That way I am not chasing hype.

I am tracking data.

And when you are trying to build equity intentionally instead of accidentally, that distinction makes all the difference.