The Promise And The Trap

You see a home listed $40,000 below market value. It looks like a steal… until it isn’t.

That is usually how the story begins.

Most people searching for the pros and cons of buying a foreclosed home are not just curious. They are trying to make sense of a process that feels confusing and risky. If you want a deeper breakdown of how the entire process works from start to finish, I explain it fully in my Foreclosure Explained: Stages, Terms, And Risks guide.

Because here is the reality.

People are searching this topic for a reason. They are trying to save money. They are trying to build equity. They are trying to invest smart in a market that feels inflated and unforgiving.

When home prices feel too high and mortgage rates make monthly payments uncomfortable, the word foreclosure starts sounding like opportunity. A shortcut. A backdoor into equity.

And sometimes it is.

Foreclosures can create opportunity.

They can also create very expensive mistakes.

Hidden repair costs. Title complications. Financing friction. Properties that look discounted on paper but end up costing more than a clean retail home down the street.

In this guide, we are going to slow this down and look at it clearly. We will cover what foreclosures are, the real pros, the real cons, and when buying one actually makes sense.

Because the goal is not to buy a cheap house.

The goal is to buy a discounted asset with manageable risk.

What Is A Foreclosed Home?

A foreclosed home is a property repossessed by a lender after the homeowner stops making mortgage payments.

That is the simple definition.

When a borrower defaults, the bank or note holder begins a legal process to recover the unpaid loan balance. If the issue is not resolved, the property is taken back and eventually sold. The goal for the lender is not to own houses. The goal is to recover as much of the loan as possible.

This is where buyers start paying attention.

Because when a bank is trying to unload an asset instead of maximize emotional value, pricing can shift. But understanding where a property sits in the foreclosure timeline matters a lot. Not all foreclosures are the same.

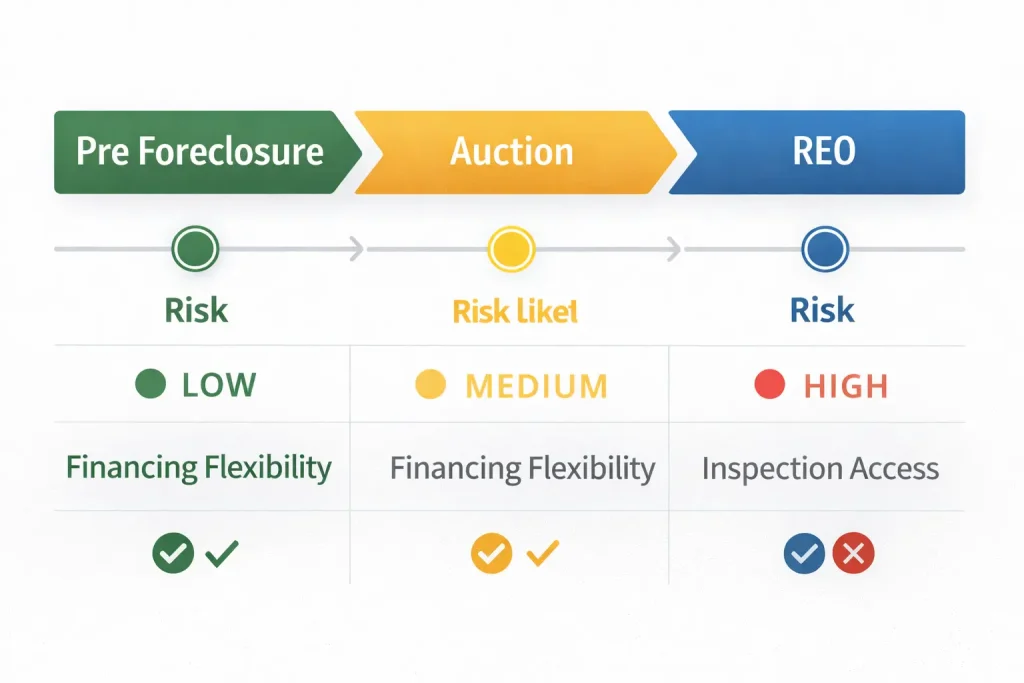

Let’s break down the three main types.

Pre Foreclosure

Pre foreclosure is the earliest stage. The homeowner is behind on payments, but the property has not yet gone to auction.

At this point, the owner still technically owns the home. They may try to sell it before the foreclosure sale date to avoid losing everything. This stage can create negotiation leverage because the seller is motivated.

Risk level here is moderate.

You can often inspect the property. You can use traditional financing in many cases. You are dealing directly with the homeowner, not the bank. There is still structure to the transaction.

But timing is critical. If you drag your feet, the property can move to auction.

Auction Or Sheriff Sale

An auction, sometimes called a sheriff sale or trustee sale, is where things get real.

This is when the property is sold publicly to the highest bidder. These sales are often held at the courthouse or online. The starting bid is usually tied to the outstanding loan amount.

Risk increases significantly at this stage.

You may not get interior access. Properties are typically sold as is. Large deposits are often required immediately. Closing windows are short. In many cases, you need cash or hard money financing.

Financing flexibility drops here. Traditional lenders usually do not move fast enough for auction timelines.

This is where inexperienced buyers can get burned quickly.

REO Or Bank Owned

If a property does not sell at auction, it becomes REO, which stands for real estate owned.

Now the bank owns it.

The lender will typically hire a real estate agent and list the property on the MLS just like a normal listing. At this stage, you can usually access the property, conduct inspections, and submit offers through standard contracts.

Risk decreases compared to auction, but it is still not the same as buying from a traditional seller.

Banks sell REO properties as is. They are not emotional. They are not attached. But they are also not generous. Negotiations can be slower and more rigid.

Here is the pattern you need to understand.

As you move from pre foreclosure to auction, risk increases.

At the same time, financing flexibility decreases.

The earlier you get involved in the process, the more options you typically have. The further you go down the foreclosure pipeline, the more experience, cash reserves, and risk tolerance you need.

That distinction alone can save you from making a very expensive decision.

The Pros Of Buying A Foreclosed Home

The biggest advantage of buying a foreclosure is simple. You can buy below market value.

But that only matters if you understand why.

Let’s walk through the real benefits without the hype.

Lower Purchase Price And Equity At Purchase

Foreclosures are often priced below comparable retail listings.

Banks do not want to own houses. They want to move non performing assets off their books and recover capital. That urgency can translate into discounted pricing, especially compared to emotional sellers who are anchored to a number in their head.

This is where the concept of equity at purchase comes into play.

Equity at purchase means you are creating margin the day you close. If similar renovated homes are selling for $300,000 and you acquire the property for $250,000 with manageable repairs, that spread is your buffer. That buffer protects you against market shifts, appraisal issues, and minor renovation surprises.

Buying right is everything.

A discounted purchase price can immediately improve your loan to value ratio, reduce risk, and strengthen your overall position. But the key word there is discounted relative to true market value, not just the list price.

Less Emotional Seller

Another overlooked advantage is who you are negotiating with.

When you buy from a traditional homeowner, there is often sentimental attachment. They raised their kids there. They remodeled the kitchen themselves. They think their house is worth more than the comps suggest.

Banks do not operate that way.

There is no emotional story attached to the property. Decisions are numbers based. If your offer aligns with their recovery goals and internal guidelines, they move forward. If it does not, they counter or decline.

Sometimes this creates less negotiation drama.

You are not arguing about paint colors or memories. You are dealing with spreadsheets. For investors especially, that clarity can be helpful.

Opportunity To Force Appreciation

One of the most powerful advantages of buying a foreclosure is the ability to force appreciation.

When a property has been neglected or poorly maintained, value is suppressed. Renovations, layout improvements, updated systems, and improved curb appeal can significantly increase resale or rental value.

You are not waiting for the market to rise. You are actively creating value.

This is why foreclosures are often targeted for flip strategies or the BRRRR method. If the numbers support it, you can renovate, raise the appraised value, refinance, and potentially recycle your capital into another deal.

But it only works if your repair estimates are realistic and your after repair value is grounded in solid comparable sales.

Investment Leverage Potential

Foreclosures can also offer strong investment leverage when purchased correctly.

If you acquire a property at a discount and stabilize it with renovations or proper management, you may unlock rental income upside that did not previously exist. Forced equity can improve refinance options. Lower acquisition cost improves cash on cash returns.

That is where real return on investment comes from.

But this is not automatic. High interest rates, rising insurance costs, and property tax reassessments can quickly erode thin margins. The deal has to work on paper before it works in real life.

The bottom line is this.

The pros of buying a foreclosed home are real. Lower entry price. Negotiation clarity. Value creation potential. Investment leverage.

Just make sure the numbers support the opportunity before you convince yourself you found a bargain.

The Cons Of Buying A Foreclosed Home

Here is the part most listing descriptions will not emphasize.

Foreclosures come with real risk.

And if you are already stretched financially, these risks can compound quickly. Let’s break down where buyers typically get burned.

Sold As Is

Most foreclosed homes are sold as is.

That means limited repair negotiations. The bank usually will not fix anything. If the inspection uncovers issues, the responsibility often falls entirely on you.

Traditional sellers sometimes agree to repair credits or concessions. Banks rarely operate that way. They price the property with condition in mind and expect the buyer to absorb the rest.

If you do not build repair margin into your numbers, you are setting yourself up for stress.

Hidden Repair Costs

The biggest financial shock usually comes from repairs.

Roof replacement alone can run $10,000 to $25,000 depending on size and materials. HVAC systems that have been sitting unused for months may fail immediately after closing and cost $5,000 to $12,000 to replace. In some distressed properties, plumbing copper has been stripped out and sold, adding thousands more in unexpected expenses.

Mold remediation is another common issue, especially in homes that have sat vacant with moisture problems. Foundation problems are even more serious and can easily exceed $15,000 to $40,000 depending on severity.

This is why due diligence matters.

Cheap upfront does not mean cheap overall. A $40,000 discount disappears quickly if you inherit $50,000 in deferred maintenance.

Financing Can Be Harder

Financing a foreclosed home is not always straightforward.

FHA loans have property condition standards. If the home has peeling paint, missing handrails, roof damage, or safety hazards, it may not qualify. Some lenders avoid heavily distressed homes entirely.

If you are bidding at auction, you may need cash or hard money financing. Traditional loans typically move too slowly for short auction closing windows.

Appraisal complications can also kill deals. If the property appraises below your purchase price due to condition or market softness, you may need to bring an additional $10,000 to $20,000 to closing just to make the deal work.

This is where many first time buyers underestimate the complexity.

Title And Legal Risks

Foreclosures can also carry legal baggage.

Outstanding property taxes may attach to the property. HOA liens can surface. In some cases, title issues create delays if ownership records are not clean.

Certain states have redemption periods where the previous owner may have the right to reclaim the property after sale by paying off the debt. This varies by state, but it is something you need to understand before proceeding.

A thorough title search and proper closing process are not optional here. They are mandatory.

Longer And More Complex Process

Finally, the process itself can be slower and more frustrating.

Banks operate through asset managers, attorneys, and internal approval systems. Responses can take longer than with individual sellers. Multiple layers of corporate bureaucracy can stall simple decisions.

You may submit an offer and wait days or weeks for a response.

If you are used to fast negotiations, this can test your patience. But patience is part of the game when dealing with institutional sellers.

The bottom line is this.

The cons of buying a foreclosed home are not theoretical. They are financial, legal, and operational realities.

If you walk in prepared, you can manage them. If you walk in chasing a discount without a buffer, they can overwhelm you quickly.

Real Numbers Example: Is It Actually A Deal?

Here is how you determine if a foreclosure is actually a deal.

You run the numbers before you get emotionally attached.

Let’s walk through a simple example.

H3 Example Scenario Breakdown

Purchase Price: $210,000

Rehab Budget: $35,000

Holding Costs: $10,000

Total Investment: $255,000

After Repair Value or ARV: $275,000

On the surface, this looks fine.

You are all in at $255,000 and comparable renovated homes are selling for $275,000. That gives you $20,000 in gross equity.

Not bad, right?

But we are not done.

If you plan to sell the property, you still have agent commissions, closing costs, transfer taxes, and potential seller concessions. Those transaction costs can easily eat up $15,000 to $25,000 depending on the price point and structure of the deal.

Now your $20,000 gross margin starts shrinking quickly.

If you are holding the property as a rental, you still need to factor in insurance increases, property tax reassessments, maintenance reserves, and vacancy. If those numbers are tight, your projected cash flow may not look nearly as strong once reality hits.

This is where many buyers miscalculate.

They focus on the difference between purchase price and ARV and forget everything in between. They forget time. They forget friction. They forget that projects rarely come in exactly on budget.

And if your rehab runs $10,000 over budget, your $20,000 cushion just got cut in half.

This is why margin matters.

Slim deals become bad deals fast.

A foreclosure only makes sense when the numbers leave room for error. Because in real estate, there is almost always some error.

When Buying A Foreclosure Makes Sense

Buying a foreclosure makes sense when you are financially and mentally prepared for volatility.

Not when you are hoping everything goes perfectly.

There are certain conditions where the risk becomes calculated instead of reckless. If these boxes are not checked, you are probably forcing the deal.

Let’s walk through them.

You Have Renovation Reserves

Foreclosures make sense when you have real cash reserves.

Not just enough to close. Enough to handle surprises.

If your rehab budget is $35,000 and you only have $35,000 available, that is not a reserve. That is a gamble. You should have additional liquidity beyond your projected repair budget so an unexpected $8,000 issue does not derail the project.

Liquidity creates breathing room.

Without it, every contractor invoice becomes stressful.

You Are Comfortable With Uncertainty

Foreclosures are not clean retail transactions.

There may be delayed responses. There may be missing documentation. There may be condition issues that were not obvious during the initial walkthrough.

If uncertainty keeps you up at night, this may not be your lane.

You need to be able to evaluate risk logically instead of emotionally. Because once you are under contract, backing out can cost time and money.

You Have A Contractor Lined Up

Foreclosures move fast once you close.

Every month you hold the property, you are carrying costs. Taxes, insurance, utilities, possibly loan payments. Time directly affects your return.

If you do not already have a contractor relationship established, you may lose weeks just getting bids. And in some markets, labor shortages can delay projects even longer.

Speed matters.

The smoother your renovation timeline, the stronger your margins stay.

You Have Built In A Repair Buffer

A solid deal includes a repair buffer of at least 15 percent to 25 percent above your estimated rehab cost.

If your projected renovation is $35,000, your real planning number should be closer to $40,000 to $44,000. That buffer protects you from hidden issues behind walls, subfloor damage, electrical surprises, or permit adjustments.

Deals rarely come in exactly on budget.

Your buffer is what separates disciplined investing from speculation.

You Are Buying Well Below ARV

The final filter is simple.

You must be buying significantly below after repair value.

If ARV is $275,000 and you are all in at $255,000, that margin is thin. But if you can acquire the property and complete renovations with a total investment of $230,000 to $240,000, that changes the risk profile entirely.

Buying below market value is not about chasing a discount.

It is about creating room for error.

Foreclosures make sense when the math protects you. If the math is tight before you start, it usually only gets tighter once real life kicks in.

When It Probably Does Not Make Sense

Buying a foreclosure does not make sense when you are financially stretched.

That is the simplest filter.

A discounted price does not fix weak fundamentals. If your personal finances are already tight, layering renovation risk on top usually creates stress instead of wealth.

Let’s be honest about where this goes wrong.

You Are Stretching Financially

If you are maxing out your debt to income ratio just to qualify, this is not the time to take on a distressed property.

Foreclosures require flexibility. Unexpected costs, timing delays, and higher insurance premiums can push monthly expenses beyond what you projected.

When your budget has no margin, every surprise becomes a problem.

And in distressed properties, surprises are common.

You Are Using A Minimal Down Payment

Minimal down payments and distressed assets are not a great combination.

Low equity positions increase risk. If the appraisal comes in low or the market softens slightly, you may not have enough equity to refinance or sell without writing a check.

Strong deals start with strong positioning.

If you are barely scraping together closing costs, you are not positioned for volatility.

You Do Not Have Cash Reserves

This is where most people get into trouble.

You cannot rely on credit cards to fix a roof. You cannot hope the next paycheck covers a $12,000 HVAC replacement. Real estate punishes undercapitalized buyers quickly.

Cash reserves are not optional in foreclosure deals.

They are your insurance policy.

You Are Emotionally Attached To Getting A Deal

Sometimes buyers become obsessed with the idea of winning.

They want to say they bought $40,000 below market value. They want to feel like they beat the system. That emotional attachment clouds judgment.

If you start justifying numbers instead of verifying them, you are already drifting away from discipline.

The strongest negotiating tactic in real estate is being willing to walk away.

If you cannot walk away, you are negotiating from weakness.

You Cannot Afford Unexpected Repairs

Ask yourself this directly.

If a foundation issue costs $18,000 more than expected, can you handle it without financial strain? If the property needs an additional $10,000 in electrical upgrades to pass inspection, can you absorb it?

If the honest answer is no, the deal is not for you.

This is where I see a major misunderstanding in the market.

Many buyers chasing cheap are not actually chasing margin. They are chasing affordability. They want the lower price because traditional homes feel out of reach.

But a foreclosure does not make a home affordable if the risk transfers to you.

A low purchase price does not equal low total cost.

If you are buying because it feels cheaper, not because the numbers are strong, you are solving the wrong problem.

Foreclosures are tools for disciplined buyers.

They are traps for financially fragile ones.

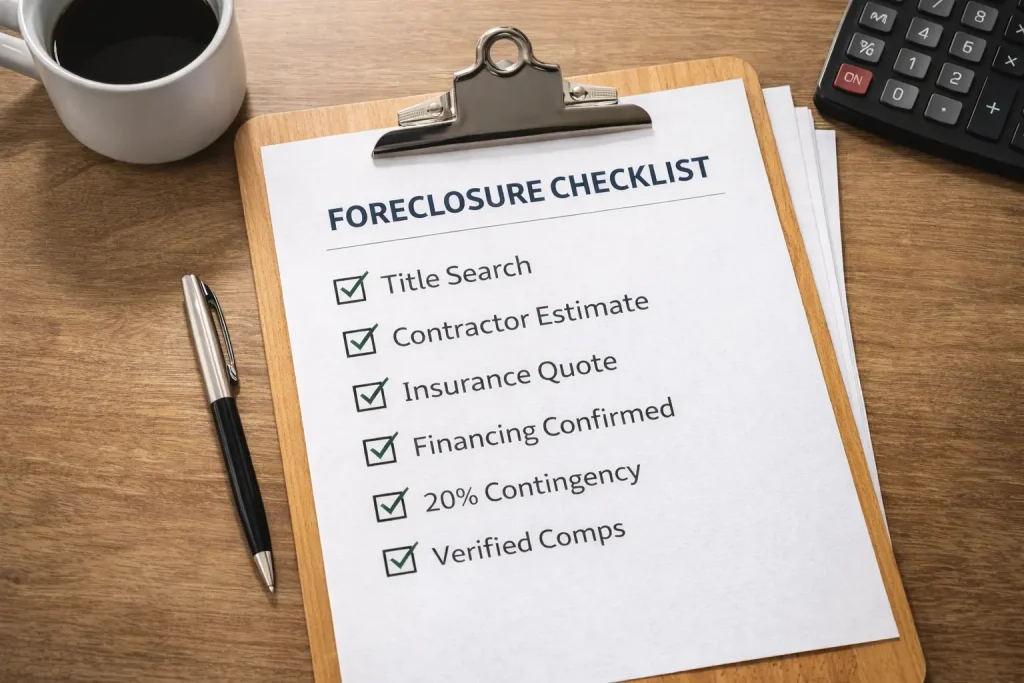

Foreclosure Buying Checklist

If you are serious about buying a foreclosure, you need a system.

Emotion will get you in trouble. A checklist keeps you disciplined.

Before you move forward, confirm every item below. If one of these is missing, slow down.

Clear Title Search Completed

Do not assume the title is clean.

Make sure a professional title search has been completed and reviewed. Confirm there are no outstanding liens, unpaid property taxes, HOA claims, or ownership discrepancies.

If there is confusion around ownership or encumbrances, you want to know before you wire funds.

Title issues can delay closings or create legal headaches that erase profit quickly.

Repair Estimate From A Contractor

Online estimates and rough guesses are not enough.

You need a written repair estimate from a licensed contractor who has physically walked the property. That estimate should break down labor, materials, and timeline.

Foreclosures often hide issues behind walls and under floors. If you do not have a real number, you do not have real math.

Hope is not a renovation strategy.

Insurance Quote Secured

Insurance premiums have been volatile in many markets.

Before buying, secure a formal insurance quote based on the property’s current condition and location. Do not assume your current policy rates apply.

Higher premiums can impact cash flow projections more than you expect. Locking in a quote removes one major unknown from the equation.

Financing Pre Approved For Distressed Property

Being pre approved is not enough.

You need confirmation that your lender is comfortable financing a distressed property in its current condition. Some loan programs have strict property standards that foreclosures may not meet.

If you are using hard money or private lending, confirm timelines and terms in writing.

Financing surprises are one of the fastest ways to lose earnest money.

Budget Includes 15 To 25 Percent Contingency

Your renovation budget must include a contingency buffer of at least 15 percent to 25 percent.

If your contractor estimate is $35,000, your planning number should reflect an additional cushion. That buffer protects you from the unknown.

Real estate rarely runs perfectly on schedule or on budget.

Your margin is your safety net.

Comparable Sales Verified

Do not rely on list prices.

Verify recent comparable sales that match the property’s size, layout, condition, and location. Look at what homes actually sold for, not what sellers hoped to get.

This determines your true after repair value and your true exit potential.

If the comps do not support your numbers, the deal does not work.

The goal of this checklist is simple.

Remove as much uncertainty as possible before you commit.

Foreclosures reward preparation. They punish shortcuts.

Final Verdict: Opportunity Or Liability?

Here is the real question.

Is this an opportunity… or a liability in disguise?

Buying a foreclosure is not about getting a cheap house.

It is about getting a discounted asset with manageable risk.

There is a big difference.

A low list price means nothing if repair costs, financing friction, insurance increases, and holding time wipe out your margin. On the flip side, a properly underwritten foreclosure with strong reserves and realistic numbers can accelerate equity faster than a traditional retail purchase.

The deal is not defined by the word foreclosure.

It is defined by the math.

If you have reserves, discipline, contractor relationships, and a real contingency buffer, foreclosures can absolutely make sense. They can create equity at purchase. They can create forced appreciation. They can create leverage.

But if you are stretching to make the numbers work, chasing the feeling of a bargain, or solving affordability by transferring risk to yourself, that same foreclosure can become expensive quickly.

This is why due diligence is everything.

Run the comps carefully. Confirm title. Secure financing. Get real repair estimates. Stress test your budget. Assume something will go wrong and build that into your plan.

Because something usually does.

If you want to go deeper into foreclosure strategy, distressed property analysis, and how to evaluate deals without getting burned, that is exactly why I built this site.

Real estate can build serious wealth.

But only when you approach it like an investor, not a bargain hunter.

Foreclosure FAQ

If you are still here, you are probably weighing the risk.

Here are the most common questions I see about the pros and cons of buying a foreclosed home, answered directly.

No, foreclosed homes are not always cheaper.

Some are priced below comparable retail listings. Others are priced aggressively and attract bidding wars. In competitive markets, investor demand can push foreclosure prices right back to market value.

The list price does not determine whether it is cheap.

Comparable sales determine that.

If similar renovated homes are selling for $275,000 and your total investment is $260,000, that may be a deal. If your total investment is $270,000, that margin is thin.

Foreclosure status alone does not guarantee a discount.

It depends on the stage.

If the property is an REO listed on the MLS, you can usually conduct inspections just like a traditional sale. In pre foreclosure, inspections are also often possible if the homeowner cooperates.

At auction, inspections are rarely allowed.

This is where risk increases significantly. Buying sight unseen is common at auctions, and that is not for inexperienced buyers.

Always confirm inspection access before committing funds.

Sometimes.

Banks price properties based on internal recovery goals, market data, and condition. In some cases, they price aggressively to move inventory. In others, they test the market and wait.

The only way to know if a foreclosure is below market value is to verify recent comparable sales.

Do not confuse a property sitting at $210,000 with being worth $210,000.

Market value is what a buyer is willing to pay and what the comps support.

Yes, it can be.

Foreclosures often carry more condition risk, financing friction, legal complexity, and timing uncertainty than traditional home purchases.

But risk is not inherently bad.

Unmanaged risk is bad.

If you have reserves, contingency buffers, verified comps, and realistic repair estimates, the risk becomes calculated. If you are undercapitalized or guessing at numbers, the risk becomes dangerous.

The property is not the problem. Preparation is.

In many cases, yes.

If the foreclosure is listed as an REO and meets FHA property condition standards, you can use FHA financing. The property must be safe, habitable, and structurally sound.

However, if the home has major defects such as roof failure, missing systems, exposed wiring, or safety hazards, it may not qualify.

Auction purchases typically require cash or hard money financing due to short timelines.

Always confirm with your lender before assuming eligibility.

The key takeaway from all of this is simple.

The pros and cons of buying a foreclosed home are real.

But the outcome depends on how disciplined you are with the numbers.