Quick Answer: Are Foreclosure Homes Cheaper?

Yes, foreclosure homes are often cheaper than traditional homes, usually selling for about 5 to 20 percent below market value. But that discount is rarely free money. The lower price usually reflects deferred maintenance, limited inspections, financing hurdles, or higher risk.

If you are new to distressed properties, I highly recommend reading my comprehensive guide on Foreclosure Explained: Stages, Terms, And Risks before going further. Understanding how foreclosures actually work will give you context for why the pricing looks attractive in the first place.

The real question is not just are foreclosure homes cheaper. The better question is whether they are cheaper after you account for repairs, closing delays, and the stress that can come with distressed property transactions.

Here is the simple breakdown most buyers are actually looking for:

| Category | Foreclosure | Traditional Home |

|---|---|---|

| Purchase Price | Often Below Market | Market Value |

| Condition | Frequently As-Is | Move-In Ready Usually |

| Inspection | Sometimes Limited | Standard Inspection |

| Negotiation | Limited Bank Flexibility | Flexible Seller |

| Risk Level | Higher | Lower |

On paper, the foreclosure wins on price.

In reality, the traditional home often wins on predictability.

And if you are already dealing with tight cash flow, limited savings, or first-time buyer stress, predictability matters more than most people realize.

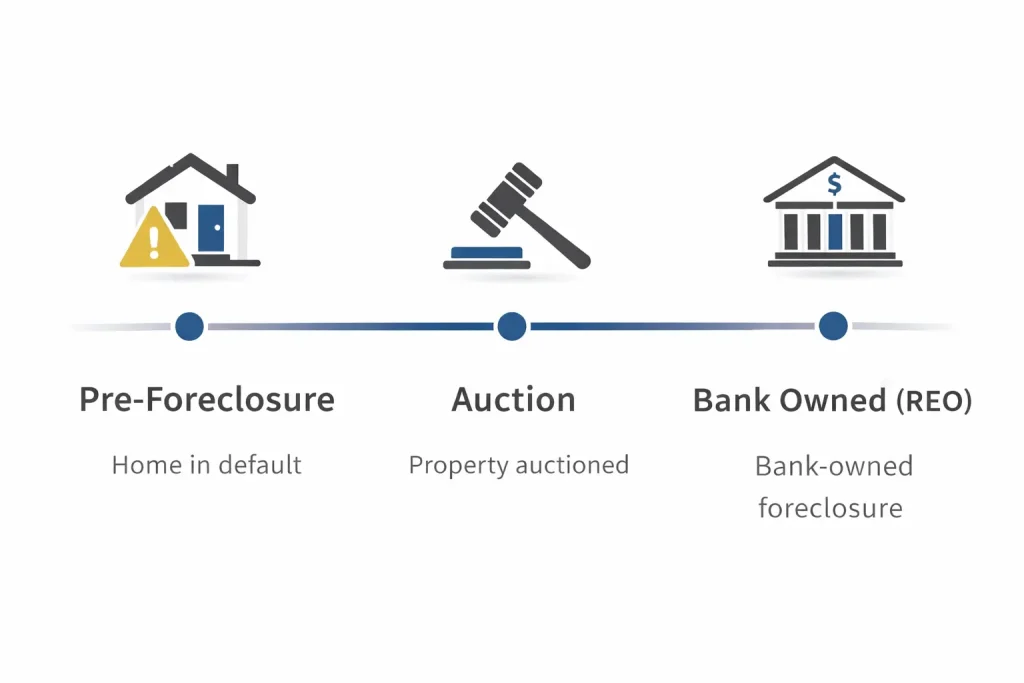

What Is a Foreclosure Home?

A foreclosure home is a property that the lender is trying to recover because the owner stopped making mortgage payments. It does not start with the bank owning the house. It starts with missed payments and escalates from there.

Understanding the stage of foreclosure matters more than most people think. The risk, financing options, and price flexibility all change depending on where the property sits in the process.

There are three main stages you need to know.

Pre Foreclosure

Pre-foreclosure is the early warning phase. The homeowner is behind on payments, but the bank has not taken the property back yet.

This is the gray area.

The owner is typically trying to avoid foreclosure altogether. That means they may be motivated to sell quickly, negotiate on price, or accept creative terms. In some cases, you can communicate directly with the homeowner and structure a deal that works for both parties.

The upside is potential negotiation leverage.

The downside is uncertainty. The property could cure the default, go into auction, or get tied up in legal delays. Timing is everything at this stage.

Foreclosure Auction

If the homeowner cannot catch up, the property moves to a public foreclosure auction. This is where things get intense.

The home is sold to the highest bidder, often at the courthouse steps or through an online auction platform. In many cases, cash or certified funds are required quickly. Financing is usually not an option.

You typically buy the property as is. Inspections are rare. Access to the interior may be limited. You are bidding based on your research, not comfort.

This is where investors show up with calculators and firm numbers. It can be profitable, but it is not for the faint of heart.

Bank-Owned REO

If no one buys the property at auction, it goes back to the lender. This is when it becomes a bank-owned property, also known as REO, which stands for real estate owned.

Now the bank is the seller.

At this stage, the property is usually listed on the open market through a real estate agent. It often shows up on platforms like Zillow and Realtor.com just like any other home. Government-owned foreclosures may also appear on HUD listings if they involve FHA-backed loans.

REOs are generally easier for regular buyers to purchase because inspections are sometimes allowed, and traditional financing may work depending on the condition.

The tradeoff is simple. The easier it is to buy, the more competition you will face.

Understanding which stage you are dealing with removes a lot of confusion. And confusion is where most first-time buyers get burned.

How Much Cheaper Are Foreclosure Homes?

Foreclosure homes are usually cheaper, but not by as much as social media makes it sound. In most cases, the discount falls somewhere between modest and meaningful depending on the market and the stage of foreclosure.

In competitive markets, you might see homes priced about 5 to 10 percent below comparable properties. In more distressed areas or softer markets, that discount can stretch closer to 10 to 20 percent.

At auctions, you may see even steeper discounts.

But the larger the discount, the higher the risk tends to be. There is almost always a reason the price looks attractive.

That is the part buyers forget when they are focused only on the sticker price.

Typical Discount Range

In a strong seller’s market, banks know what they have. They are not giving properties away.

You may see a small price advantage compared to similar homes on the MLS, usually in that 5 to 10 percent range. That might help you compete in a tight affordability environment, especially if high mortgage rates are already stretching your budget.

In weaker markets or neighborhoods with higher distress, you may find discounts closer to 15 or even 20 percent. These are typically properties with visible condition issues or longer days on market.

Auction properties can sometimes sell at deeper discounts.

But remember, auction deals often require cash, fast closings, and limited due diligence. That is not a discount. That is risk priced into the deal.

Why They’re Discounted

Foreclosure homes are discounted because the situation is imperfect.

The most common reason is the property condition. Many foreclosures are sold as is. Deferred maintenance, outdated systems, roof issues, plumbing problems, or cosmetic neglect are common. Repairs are the hidden equalizer.

Banks also want fast liquidation. They are not emotionally attached to the property. Their goal is to recover as much of the unpaid loan balance as possible and move on. Speed often matters more than squeezing out every last dollar.

There is also uncertainty. The property could have occupancy issues, unpaid liens, HOA balances, or title complications. These risks scare away some buyers, which pushes the price lower.

Limited seller disclosures add another layer. Unlike traditional sellers, banks typically provide minimal information about the property’s history.

All of this creates a price discount.

But it also creates work.

A Real World Example

Let’s run the numbers because this is where clarity matters most.

- Market Value: 400,000

- Foreclosure Price: 350,000

- Estimated Repairs: 30,000

- Total Investment: 380,000

- True Discount: 20,000, which equals 5 percent

On paper, the home looked 50,000 cheaper than market value.

In reality, after repairs, the true savings shrank to 20,000.

That is still a discount.

But it is not life-changing money. And if repairs run over budget, that margin can disappear quickly.

This is where many first-time buyers miscalculate. They focus on the headline discount instead of the total cost.

If you are already tight on savings or do not have a strong emergency cushion, even a small repair surprise can erase the perceived advantage.

So yes, foreclosure homes can be cheaper.

But the only number that matters is the all-in number.

When Foreclosures Are Actually a Good Deal

Foreclosures are a good deal when you are financially prepared and emotionally disciplined. They are not a shortcut to easy equity. They are a calculated move.

If you are stretching to buy the property in the first place, it is probably not the right play. But if you have margin, patience, and a clear plan, the math can absolutely work in your favor.

Here is when a foreclosure actually makes sense.

✔ You Have a Renovation Budget

The biggest mistake I see is buyers using every dollar for the down payment and then hoping nothing breaks.

Hope is not a strategy.

If you are buying a foreclosure, you should have real cash reserves set aside for repairs. Not just cosmetic touch-ups. I am talking about roofs, HVAC systems, plumbing, and electrical panels. The stuff that actually moves the needle.

Many buyers underestimate irregular expenses, and that is exactly how people end up back in credit card debt, trying to patch a house together.

If you have reserves, the discount becomes an opportunity.

If you do not, it becomes stress.

✔ You Understand As-Is

As is does not mean cosmetic flaws. It means the seller is not fixing anything.

You have to price the risk up front. That means running conservative repair numbers. That means assuming something will cost more than expected. That means building in a buffer.

If the numbers still work after padding your repair estimate, you are thinking like an investor.

If the deal only works in a perfect scenario, you are gambling.

Foreclosures reward realism. They punish optimism.

✔ You Are Buying for Long-Term Equity

Foreclosures make the most sense when you are playing the long game.

If you plan to live in the property for years or hold it as a rental, small short-term price fluctuations matter less. You are building equity over time while improving the property.

Trying to flip immediately in a tight margin environment can be dangerous. Holding costs, slower resale timelines, and market shifts can eat your profit.

Long-term ownership gives you breathing room.

Short-term speculation increases pressure.

✔ You Are Competing Smartly

A good deal can turn into a bad deal fast when ego gets involved.

At auctions, especially, it is easy to get caught up in bidding wars. Investors push the price up. Emotions creep in. Suddenl,y the discount disappears.

You need a number before you ever raise your hand.

If the bidding goes past your limit, you walk away. No hesitation.

The strongest position in real estate is the ability to walk away and mean it.

Foreclosures are not good deals because they are foreclosures.

They are good deals when the numbers work, the risk is understood, and you have the financial stability to absorb surprises.

When Foreclosures Are NOT Cheaper

Foreclosures are not cheaper when the hidden costs outweigh the purchase discount. The listing price might look attractive, but if the underlying problems are expensive enough, the deal disappears quickly.

This is where a lot of first-time buyers get blindsided.

They assume a lower price equals better value. But value only exists if the numbers still make sense after everything is accounted for.

Here are the situations where foreclosure math breaks down.

❌ Major Structural Issues

If the property needs a new foundation, roof, or HVAC system, the discount can vanish overnight.

Cosmetic updates are one thing. Paint and flooring are manageable. Structural problems are a different category entirely. Foundation repairs alone can run into tens of thousands of dollars. A full roof replacement or new HVAC system can easily wipe out any perceived savings.

This is where poor inspections hurt buyers the most. Hidden issues like roof leaks or foundation cracks often surface late in the process, and by then, emotions are already involved.

If the repair scope is large and you do not have deep reserves, the foreclosure is not cheaper. It is just a deferred expense.

❌ Hidden Liens or Legal Problems

Unpaid property taxes, HOA dues, utility bills, or other liens can attach to the property.

If you skip proper due diligence or rush through the title process, you could inherit someone else’s financial mess. These issues can delay closing or require you to bring additional funds to clear title.

Banks do not always volunteer this information upfront. And at auction, you may have even less clarity.

Legal complications increase uncertainty.

And uncertainty increases cost.

❌ Financing Challenges

Not every foreclosure qualifies for traditional financing.

Some lenders will not approve loans on distressed properties that fail minimum condition standards. That means peeling paint, exposed wiring, missing appliances, or water damage can derail your approval.

You might need cash or alternative financing.

And alternative financing often comes with higher rates, shorter terms, and stricter conditions.

If your budget is already tight and you are relying on specific loan programs to qualify, this can create serious stress. A cheap house that cannot be financed is not a deal.

❌ Overbidding at Auction

Auctions attract competition.

Individual investors, institutional buyers, and experienced flippers show up with firm numbers and cash ready to move. It is easy to get caught up in the energy and push your bid beyond your limit.

Once you overpay, the built-in discount disappears.

At that point, you are no longer buying a foreclosure at a discount. You are buying a risky property at market value.

The bottom line is simple.

Foreclosures are not automatically cheaper.

They are only cheaper when the price reflects the true condition, legal standing, financing reality, and competitive landscape of the property.

Foreclosure vs Traditional Home: Total Cost Comparison

Foreclosures often look cheaper at first glance, but the total cost is what actually matters. The purchase price is only one piece of the equation.

If you are trying to protect your cash flow, avoid debt stress, and build equity the smart way, you have to zoom out. A lower list price does not automatically mean a lower total investment.

Let’s break this down clearly.

Purchase Price

This is where foreclosures usually win.

They are often listed below comparable traditional homes in the same neighborhood. That price difference is what draws buyers in.

But price alone is incomplete information. It tells you what you pay today, not what you will spend tomorrow.

Inspection and Appraisal

Traditional homes typically allow full inspections and standard appraisal timelines. That means fewer surprises.

Foreclosures can be different.

Some allow inspections. Some limit access. Auction purchases may not allow inspections at all before closing. Appraisals can also be more challenging if the property condition is borderline.

Less clarity increases risk.

Repairs

Repairs are the biggest variable in the foreclosure equation.

A traditional home may need minor updates. A foreclosure may need mechanical systems replaced, roof repairs, plumbing fixes, or code corrections.

If you underestimate repairs, the savings shrink quickly.

This is where many buyers undercalculate. They focus on cosmetic updates but ignore long-term capital expenditures.

Carrying Costs

Time is money in real estate.

If a foreclosure requires renovation before move-in or resale, you are carrying property taxes, insurance, utilities, and possibly loan payments during that time.

The longer the project drags out, the more those monthly expenses add up.

Traditional homes usually involve shorter timelines and faster occupancy.

Financing Terms

Traditional financing is typically cheaper and more predictable.

Foreclosures in rough condition may require cash or alternative loan products. Hard money or private loans often come with higher interest rates and shorter repayment windows.

Even a small rate difference over time can impact your overall cost.

If financing becomes more expensive, the initial discount loses some of its advantage.

Time to Close

Traditional sales usually follow a structured timeline.

Foreclosures can move fast at auction or move slowly during bank negotiations. Delays, paperwork issues, or title complications can extend the process.

Delays create uncertainty. And uncertainty can create additional costs.

Cheaper upfront does not always mean cheaper overall.

The cleaner way to think about this is with a simple formula:

True Cost = Purchase Price + Repairs + Holding Costs + Risk Premium

That risk premium is real.

It includes unexpected repairs, legal surprises, financing friction, and emotional stress. The more uncertainty involved, the higher that premium should be in your calculations.

If the numbers still work after accounting for all of that, the foreclosure may be a strong move.

If not, the traditional home might quietly be the better financial decision.

Can First-Time Buyers Buy Foreclosures?

Yes, first-time buyers can buy foreclosures. The bigger question is whether they should.

There is a myth floating around that foreclosures are reserved for cash-heavy investors. That is not entirely true. The reality is more nuanced, and it depends heavily on the stage of foreclosure and the property’s condition.

If you are already dealing with first-time buyer stress, tight savings, and fear of hidden ownership costs, clarity here matters.

Let’s clear up the common misconceptions.

FHA Loans May Work Depending on Condition

Many people assume FHA financing is automatically off the table for foreclosures.

That is not always the case.

If the property meets minimum property standards, FHA loans can absolutely work. The home must be safe, structurally sound, and livable. Major safety hazards, missing mechanical systems, or severe damage can derail approval.

In some situations, buyers may use renovation loan programs to finance both the purchase and repairs. But that requires patience, paperwork, and lender cooperation.

The condition of the property is the deciding factor, not the foreclosure label itself.

Inspections Are Sometimes Allowed

At the REO stage, inspections are often allowed.

Once the property becomes bank-owned and is listed on the open market, it behaves more like a traditional sale. You can typically schedule a showing, hire a home inspector, and include contingencies in your contract.

Auction purchases are different. Inspections are usually not permitted before bidding.

Understanding the stage determines how much protection you get.

Not All Foreclosures Require Cash

Cash is common at auctions, but not mandatory in every foreclosure scenario.

Pre-foreclosure and REO properties are often financed with conventional, FHA, or other loan types if the home qualifies. The idea that every foreclosure is cash only is outdated.

That said, distressed properties that fail lender condition standards may still require alternative financing or significant down payments.

Financing is possible. It just depends on the numbers and the condition.

Banks Negotiate Differently Than Private Sellers

Negotiating with a bank is not the same as negotiating with a homeowner.

Banks are less emotional. They operate on internal systems, asset managers, and predetermined thresholds. They may not respond quickly, and they rarely make repairs.

Private sellers might negotiate based on personal circumstances. Banks negotiate based on recovery strategy and timelines.

You need patience.

You also need clean paperwork and strong proof of funds or pre-approval. Banks want certainty more than charm.

The bottom line is this.

First-time buyers can buy foreclosures.

But if your budget is tight, your emergency fund is thin, and you are relying on everything going perfectly, you may want to think carefully before stepping into a distressed property situation.

Risks of Buying a Foreclosure

Foreclosures come with risk. That risk is the reason the discount exists in the first place.

If you remove the risk, you usually remove the deal.

The key is not avoiding risk entirely. The key is pricing it correctly and making sure your financial situation can absorb it. If you are living paycheck to paycheck or stretching your debt-to-income ratio just to qualify, these risks hit harder.

Here is what you need to look out for.

Deferred Maintenance

Deferred maintenance is the most common issue.

When homeowners fall behind on payments, repairs are usually the first thing to get ignored. Roof leaks sit longer. HVAC systems go unserviced. Minor plumbing problems become major ones.

You may walk into a house that looks fine cosmetically but has aging systems nearing failure.

The longer maintenance is delayed, the more expensive it becomes.

Vandalism

Vacant homes attract problems.

Broken windows, stolen appliances, damaged drywall, and missing copper wiring. I have seen it all. Once utilities are shut off and the home sits empty, it becomes vulnerable.

Even small acts of vandalism add up quickly.

This is especially common between the auction stage and the REO listing phase.

Mold

Mold is one of the most expensive and stressful issues to deal with.

If a home has been vacant with poor ventilation, roof leaks, or plumbing failures, moisture can build up quickly. Mold remediation is not cheap, and lenders often require it to be resolved before closing.

Beyond cost, there are health implications.

If you smell musty odors or see discoloration on ceilings and walls, you need to dig deeper.

Plumbing Damage

When utilities are shut off, plumbing systems can suffer.

In colder climates, frozen pipes can burst. In other cases, long-term neglect leads to corroded lines, slow leaks, or sewer line issues.

Plumbing problems rarely show their full scope during a quick walkthrough.

This is where proper inspection and conservative budgeting matter.

Utility Shutoffs

Many foreclosures have had utilities disconnected for months.

No power. No water. No heat.

That makes it harder to fully test systems during inspection. You may not know if the furnace works, if outlets are live, or if water pressure is consistent until after closing.

Uncertainty increases the risk premium.

Emotional Seller History

There is also a human side to foreclosures.

These properties often come from financial distress, job loss, divorce, or medical hardship. That emotional weight can show up in the condition of the home.

Sometimes owners stop caring. Sometimes they intentionally damage the property out of frustration. Sometimes they leave belongings behind.

You are stepping into someone else’s unfinished story.

This is why risk-adjusted decision-making matters.

You do not evaluate a foreclosure based only on price per square foot. You evaluate it based on whether the discount compensates you for the uncertainty.

If the margin between market value and total cost is thin, the risk may not be worth it.

If the margin is wide and you have reserves, patience, and a plan, the risk can be justified.

The smartest buyers are not the ones who chase the biggest discount.

They are the ones who understand what that discount is actually paying them for.

3 Question Test Before Buying a Foreclosure

Before you submit an offer or raise your hand at an auction, run this simple test. It will save you more stress than any spreadsheet ever could.

Foreclosures are not just about finding a discount. They are about managing uncertainty. If you cannot handle uncertainty financially or emotionally, the deal can turn on you fast.

Ask yourself these three questions honestly.

Do I Have 10 to 15 Percent of the Purchase Price in Cash Reserves?

If the answer is no, pause.

Not your down payment. Not your closing costs. I am talking about separate liquid reserves sitting in a savings account.

If you are buying a 350,000 dollar foreclosure, you should realistically have 35,000 to 50,000 available as a cushion. That covers repairs, surprises, holding costs, and unexpected delays.

Many buyers underestimate expenses and then end up back in credit card debt, trying to stabilize the property.

If your emergency fund is already thin, adding renovation risk on top of that can create serious money anxiety.

Am I Comfortable Managing Repairs?

Repairs are not just financial. They are logistical.

Are you comfortable coordinating contractors, getting bids, pulling permits if needed, and dealing with delays?

Do you have the time and mental bandwidth?

Owning a home already comes with responsibility. Owning a distressed home multiplies it.

If the idea of managing repairs makes you uneasy, a move-in-ready traditional home might give you more stability.

Does the Math Still Work if Repairs Run 20 Percent Higher?

This is the stress test.

If you estimate 30,000 in repairs, what happens if it turns into 36,000 or 40,000?

Does the deal still make sense?

Or does your margin disappear completely?

Conservative buyers win in real estate. Optimistic buyers get squeezed.

If the numbers only work in a perfect scenario, it is not a strong deal.

If you answered no to any of these questions, a traditional home may be safer.

There is nothing wrong with choosing predictability over complexity.

Foreclosures reward preparation. Traditional homes reward stability.

The smartest move is the one that protects your long-term financial position, not the one that looks flashy on paper.

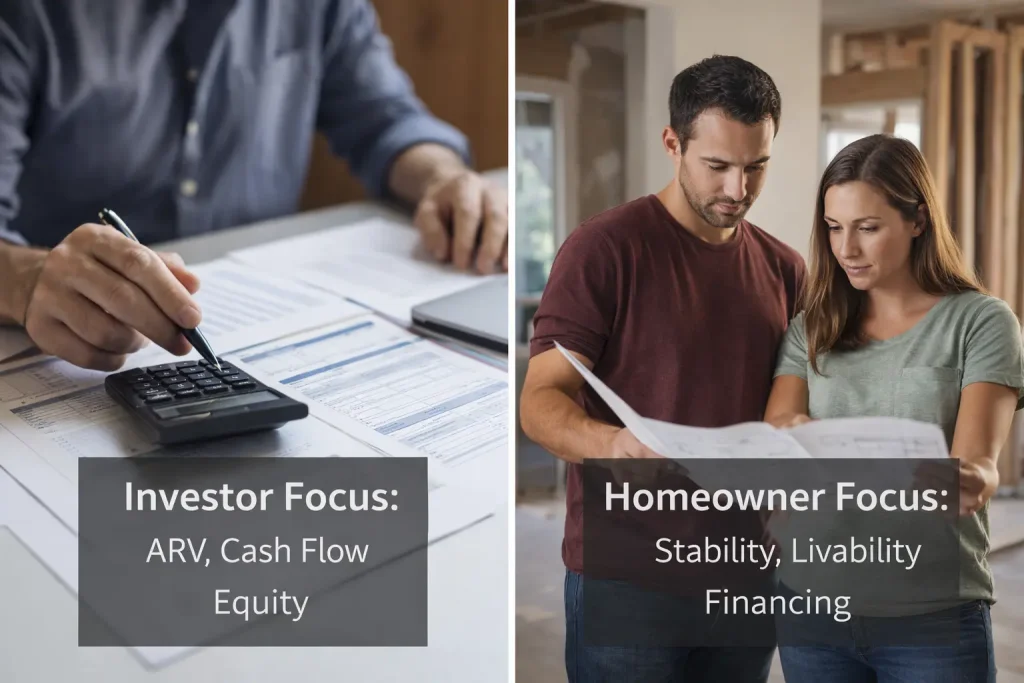

Investor Perspective vs Homeowner Perspective

Foreclosures mean different things to different buyers. An investor and a primary homeowner are not analyzing the same risk.

The mistake happens when a primary buyer evaluates a foreclosure like an investor without having investor margins or reserves.

You have to know which lane you are in before you move forward.

From the Investor Perspective

Investors care about numbers first and emotion second.

The main focus is on equity margin. How much spread exists between the purchase price and the property’s true value after improvements? If that margin is wide enough, the deal works.

After repair value, also known as ARV, is central. An investor estimates what the property will be worth once renovated and compares that to the total investment. If the gap is large enough, the risk is justified.

Rent potential and cash flow also matter. If the property can generate consistent income after expenses, insurance, taxes, maintenance, and vacancies, then the foreclosure may be a strong long-term asset.

Investors expect repairs. They expect delays. They budget for surprises.

They are buying a financial instrument.

From the Primary Homeowner Perspective

Primary buyers look at the same property very differently.

The first question is the livability timeline. Can you move in immediately? Or will you be living in a construction zone for months?

Emotional stress matters more than people admit. Managing contractors while working a full-time job and juggling life responsibilities is not easy.

Financing approval is also a bigger variable. If the property condition jeopardizes loan approval, the deal can fall apart late in the process. That creates anxiety, especially for first-time buyers.

Renovation capacity is the final filter. Do you have the time, skills, and savings to handle a property that needs work?

If the answer is no, then the foreclosure discount may not compensate you for the added complexity.

Investors buy based on margin.

Homeowners should buy based on stability.

Understanding which perspective applies to you can prevent a very expensive mistake.

Final Verdict: Are Foreclosure Homes Cheaper?

Yes, foreclosure homes are often cheaper on paper. The listing price is typically below comparable traditional homes, and that initial discount is what attracts buyers in the first place.

But they are not always cheaper in total cost.

Once you factor in repairs, holding costs, financing hurdles, inspection limitations, and uncertainty, the margin can shrink quickly. In some cases, it disappears entirely.

This is why focusing only on price per square foot is a mistake.

Foreclosures are best suited for buyers who have liquidity. You need real cash reserves beyond your down payment and closing costs. If an HVAC system fails or a roof needs replacement, you cannot be scrambling.

They are also best for buyers who understand renovation math. That means estimating conservatively, building in buffers, and stress testing the numbers before committing.

And finally, they are best for people who can tolerate uncertainty. Delays happen. Surprises happen. Negotiations with banks move differently from traditional sellers.

If you are financially stable, patient, and numbers-driven, a foreclosure can be a strategic move.

If you are stretching to afford the purchase and hoping everything goes smoothly, a traditional home may quietly be the safer and smarter path.

The discount is real.

The risk is real, too.

Your job is to decide whether the reward compensates you for that risk.