The deal looked great on paper. The purchase price made sense, the comps supported it, and the projected profit felt conservative. Then month six hit, the property was still being held, and the profit was gone without anything dramatic ever happening.

That is how most real estate deals actually fail. Not from buying too high or a surprise repair, but from time. Holding costs do not kill deals loudly. They bleed them slowly, month after month, while investors focus on the wrong variables.

This is also where most people misuse or misunderstand the tools they rely on to analyze deals. Price calculators and ARV estimates are easy to find, but very few investors slow down and use the same level of rigor when stress testing timelines and ownership drag. The difference between amateurs and professionals often comes down to whether they are using the same real estate investing tools pros rely on to evaluate risk before making an offer.

This usually starts with underestimating ownership costs. Property taxes reset higher after purchase. Insurance jumps. Utilities run longer than expected. Financing costs stack up while you wait for contractors, appraisers, tenants, or buyers. By the time people realize what is happening, the damage is already done.

If you want to avoid that outcome, you need to understand how to calculate holding cost before you ever make an offer. Not roughly. Not optimistically. Precisely enough that delays do not catch you off guard.

What Is a Holding Cost in Real Estate?

Holding cost is the money you spend simply because time is passing while you own a property. If you want a plain English definition, holding costs are the expenses that exist even when nothing is happening and no income is coming in.

This is the part of real estate most people misunderstand. They focus on the deal price and the end value, but forget about the cost of waiting in between. If a property is not stabilized yet, time itself becomes an expense.

Understanding how to calculate holding cost correctly starts with separating it from other numbers that often get lumped together.

Purchase Price vs Operating Expenses vs Holding Costs

The purchase price is what you pay to acquire the property. That number is fixed once you close. It matters, but it is not what usually kills a deal.

Operating expenses are the ongoing costs after a property is stabilized and producing income. Think property management, routine maintenance, and long term repairs. These costs are planned around rent or cash flow.

Holding costs are different. They are time based costs that exist while the property is in limbo. No tenant yet. No buyer yet. No refinance completed yet. You are owning the property, but it is not doing its job.

This includes things like loan interest, property taxes, insurance, utilities, HOA dues, and basic maintenance. None of these stop just because your timeline slipped. The longer you hold, the more they accumulate.

If you do not separate these three categories, your numbers will always look better on paper than they do in real life.

When Holding Costs Actually Apply

Holding costs are not limited to flips, even though that is where people notice them first. They apply anytime a property is not fully stabilized.

Fix and flip deals feel the impact immediately because there is no income to offset the costs. Every extra month directly reduces profit.

BRRRR projects carry holding costs during rehab, lease up, and refinance delays. A slow appraisal or tenant placement can quietly destroy returns.

Vacant rentals still have taxes, insurance, and utilities running. New builds accumulate costs during construction and delays. Long vacancies extend the holding period far beyond what most investors plan for.

If a property is not generating reliable income yet, holding costs are active. Ignoring that reality is how solid looking deals slowly turn into expensive lessons.

Why Holding Costs Are the Number One Silent Deal Killer

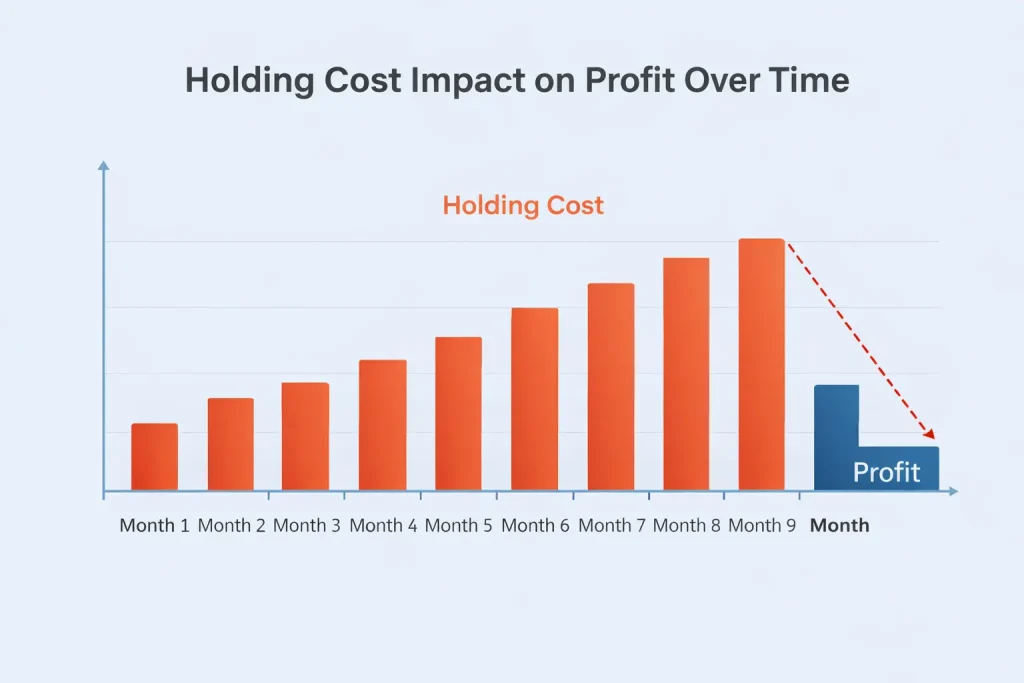

Holding costs destroy more real estate deals than bad purchase prices ever will. They do it quietly, over time, without triggering the usual red flags investors look for.

The reason is simple. Holding costs do not feel dangerous in the moment. They show up as manageable monthly numbers. But month after month, those costs stack on top of each other until the margin you thought you had is gone.

This is why understanding how to calculate holding cost accurately is not optional. It is the difference between a deal that survives delays and one that only works on paper.

Holding Costs Compound Every Month You Miss Your Timeline

Holding costs do not pause. They compound with time, regardless of progress. Even if work is happening, the clock keeps running.

One extra month can wipe out 10 to 30 percent of profit on thin margin deals. On tighter flips or leveraged projects, it can be even worse. That is before accounting for price reductions, incentives, or market shifts.

Rising interest rates make this problem far more severe. Higher financing costs mean each additional month is more expensive than the last. What used to be a small delay now carries real financial weight.

The takeaway is simple. Time is not neutral in real estate. Time costs money, and the bill grows the longer you wait.

Why Pro Formas Almost Always Underestimate Holding Costs

Most pro formas are built on optimistic timelines. They assume smooth renovations, fast lease ups, and immediate refinances or sales.

In reality, projects stall. Contractors get delayed. Appraisals come in low. Buyers hesitate. Tenants take longer to place. Each delay extends holding costs without increasing revenue.

Pro formas rarely stress test these scenarios. They show the best case, not the most likely case. That gap is where deals fail quietly.

If your deal only works when everything goes perfectly, it is not a strong deal. It is a fragile one.

The Most Common Holding Cost Mistakes Investors Make

The most dangerous phrase in real estate is it will only take three months. That assumption is responsible for more blown budgets than any other.

Another common mistake is ignoring opportunity cost. Cash tied up in a stalled project is cash that cannot be used elsewhere. That lost flexibility has a real cost, even if it does not show up on a spreadsheet.

Finally, many investors assume instant stabilization. They expect tenants to appear immediately or buyers to move quickly. Markets do not work on investor timelines.

Holding costs punish optimism. They reward realism. If you plan for delays instead of hoping they will not happen, your deals have a chance to survive.

The Core Holding Cost Formula for Real Estate Deals

Holding costs are not complicated, but they are often misunderstood. At its core, holding cost is a time based calculation. You are measuring how much each month of ownership costs you while the property is not fully stabilized.

If you want to understand how to calculate holding cost correctly, you need to think in months, not years. Real estate deals do not fail annually. They fail one delayed month at a time.

The Basic Holding Cost Formula

The simplest way to calculate holding cost looks like this.

Total holding cost equals monthly holding cost multiplied by the number of months held.

This formula works because it forces you to confront the variable that actually matters. Time. Every additional month adds another full set of expenses to the deal.

If your timeline slips from four months to six, you did not just add two months. You added two full cycles of costs that were never part of the original plan.

This is why even small delays can have outsized consequences.

The Expanded Monthly Holding Cost Formula

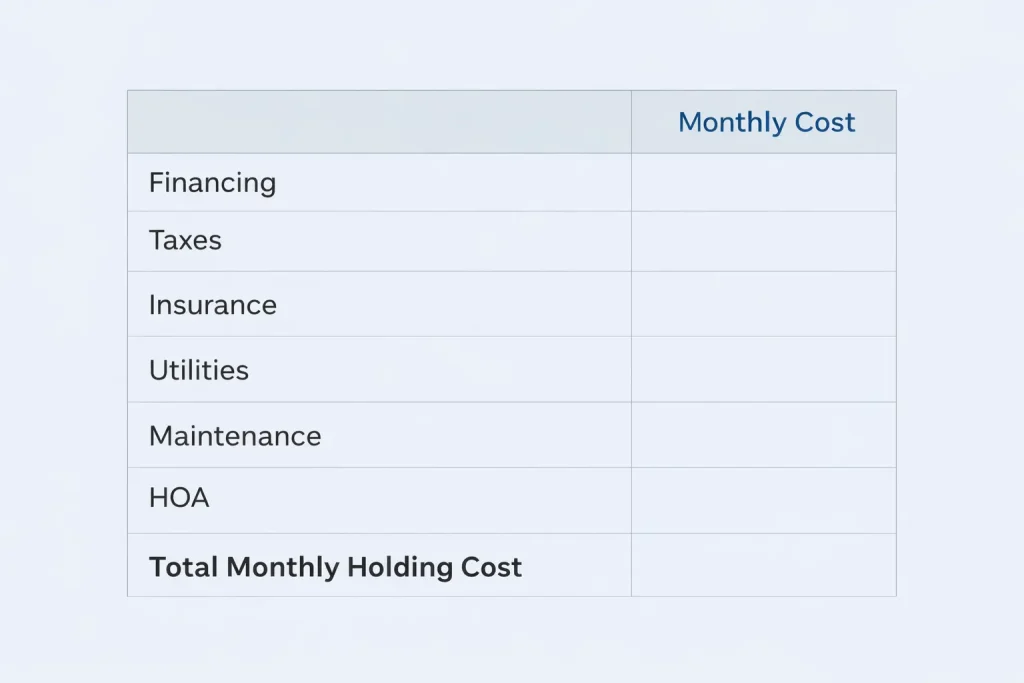

Monthly holding cost is the sum of all expenses that continue while the property produces no meaningful income.

That includes financing, property taxes, insurance, utilities, maintenance, HOA fees, and vacancy related costs. If the expense exists simply because you own the property, it belongs here.

Notice what is missing. Renovation costs are not holding costs. Purchase price is not a holding cost. These numbers matter, but they do not grow just because time passes.

Holding costs grow because ownership continues.

Why Monthly Clarity Matters More Than Annual Estimates

Annual numbers hide risk. Monthly numbers expose it.

When investors think annually, holding costs feel abstract and distant. When they think monthly, the pressure becomes real. A six hundred dollar monthly hold does not sound dangerous until it repeats six times in a row.

Monthly clarity also makes timeline slippage obvious. You can see exactly how much each delay costs you, rather than discovering the damage after the deal is already weak.

Why Time Assumptions Are the Real Risk Variable

Most deals fail because of incorrect time assumptions, not bad math. The cost per month is usually known. The duration is not.

Every holding cost calculation should start with a conservative timeline and then be stress tested with delays. If the deal breaks with one extra month, it was never strong to begin with.

Time is the lever that amplifies holding costs. Control your assumptions there, and the rest of the math becomes much easier to trust.

Line by Line Breakdown of Real Estate Holding Costs

Holding costs feel small when viewed individually. The problem is that every one of these expenses runs at the same time, every month, while the property is not stabilized. This is where most investors underestimate how expensive waiting really is.

Below is a clean, line by line breakdown of the costs that matter when learning how to calculate holding cost correctly.

Financing Costs

Financing is usually the largest holding cost and the fastest way profit erodes.

Mortgage interest continues whether the property is occupied or not. Hard money interest is even more aggressive, often compounding monthly at high rates. Points paid upfront should be amortized across the expected hold period so you see their true monthly impact.

Construction loans accrue interest as funds are drawn, which means delays increase costs even if work is incomplete. Then there is opportunity cost. Cash tied up in a stalled project cannot be used elsewhere, and that lost flexibility has a real price even if it never appears on a statement.

Financing costs punish slow timelines more than any other category.

Property Taxes

Property taxes are rarely as predictable as investors assume.

Taxes should always be calculated on a monthly, prorated basis. Many markets reassess shortly after purchase, especially when a property changes hands. That reassessment can push taxes up significantly, right in the middle of your hold.

Vacant properties can also trigger higher tax rates or penalties in certain municipalities. These increases often catch investors by surprise because they do not appear in initial projections.

Taxes are quiet, persistent, and impossible to pause.

Insurance

Insurance costs increase the moment a property becomes vacant.

Vacant property insurance is more expensive because insurers view empty homes as higher risk. Builder’s risk policies add another layer of cost during renovations or new builds.

Higher premiums are not optional. They are required to maintain coverage, satisfy lenders, and avoid catastrophic exposure. Many deals underestimate this line item because the increase feels small until it repeats month after month.

Insurance does not care if progress is happening.

Utilities

Utilities are easy to overlook and easy to underestimate.

Electric, gas, water and sewer, and trash all continue during vacancy. Internet is often forgotten entirely, even though it is commonly required for security systems, contractors, or remote monitoring.

Individually, these costs feel minor. Together, they add hundreds per month while the property produces nothing.

Utilities are a perfect example of how small leaks sink deals over time.

Maintenance and Security

Vacant properties still require care.

Lawn care, snow removal, pest control, and basic upkeep are necessary to avoid code violations, fines, or neighborhood complaints. Deferred maintenance during vacancy often leads to larger problems later.

Security related upkeep is part of this category as well. An unmaintained property attracts attention for the wrong reasons.

Neglect increases risk and extends timelines, compounding holding costs further.

HOA and Municipal Fees

HOA dues continue regardless of occupancy. Special assessments can appear without warning and immediately impact holding costs.

City inspections, permits, and reinspection fees also fall into this category. Delays caused by municipal processes often cost money twice, once in fees and again in extended holding time.

These costs are rarely negotiable and often ignored in early projections.

Vacancy and Lease Up Drag

Even after renovations are complete, holding costs do not stop.

Post renovation vacancy is normal. Tenant placement takes time. Units need to be rent ready, marketed, and shown. Every day without a tenant extends the holding period.

Assuming instant occupancy is one of the most common mistakes investors make. Lease up drag should always be included when calculating holding costs.

If income has not started, the clock is still running.

Real World Example of Holding Cost on a $300,000 Property

Seeing the math laid out is where holding costs stop feeling abstract. Once you run a real scenario, it becomes obvious how quickly profit disappears when timelines slip.

This example shows how to calculate holding cost on a typical $300,000 property and why small delays matter more than most investors expect.

Scenario Setup

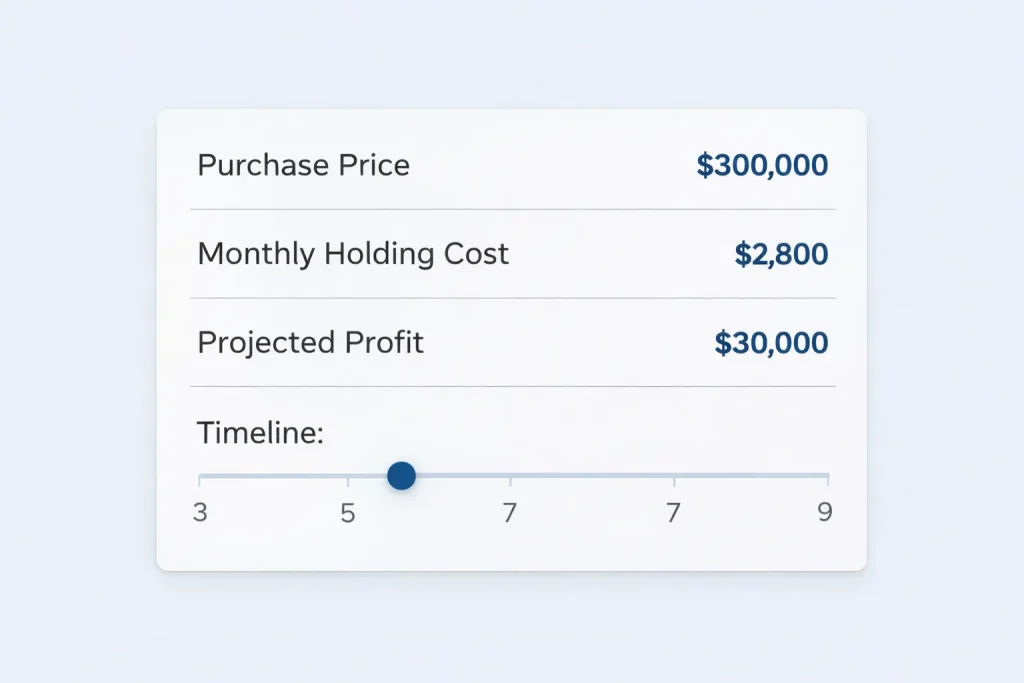

Assume a $300,000 purchase price on a distressed property.

The deal is financed with a short term loan, typical of a flip or BRRRR project. The property is vacant and not producing income during renovation. The original plan assumes a three month timeline from purchase to sale or refinance.

This is a realistic setup. It is also where optimism usually creeps in.

Everything below assumes no major surprises. Just normal ownership costs while time passes.

Monthly Holding Cost Breakdown

Here is what the monthly holding cost might realistically look like.

Financing costs come in at $1,600 per month based on interest only payments. Property taxes average $350 per month once prorated. Insurance runs $200 per month due to vacancy. Utilities total $300 per month. Maintenance and basic upkeep add another $200. HOA dues add $150.

That brings total monthly holding cost to approximately $2,800.

This is the number most investors underestimate. It does not feel dangerous until it repeats.

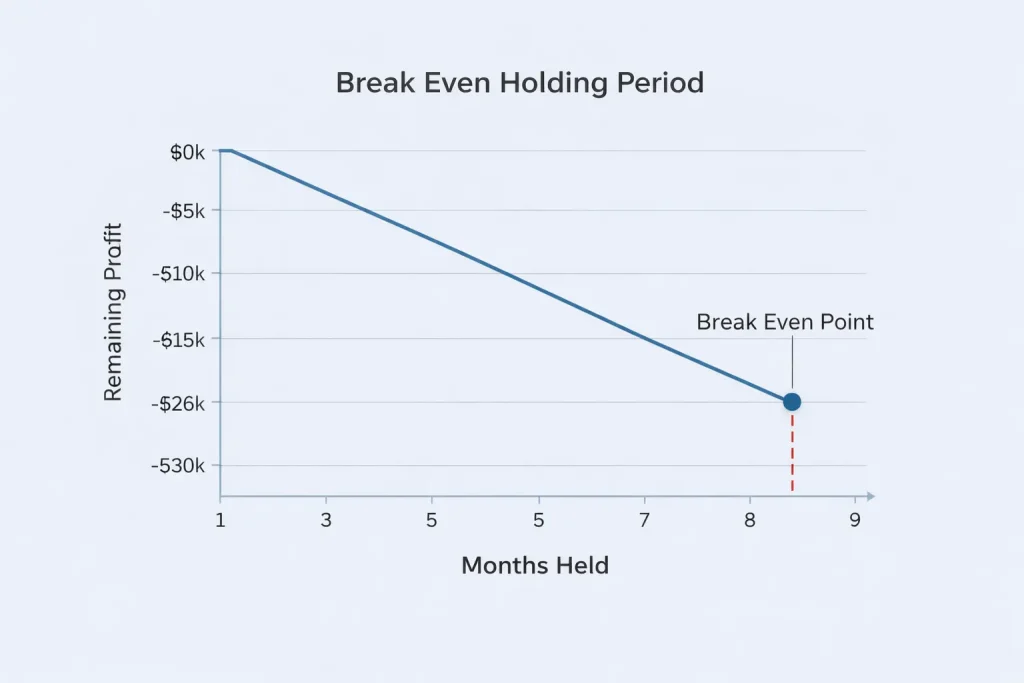

Timeline Stress Test and Profit Erosion

At a three month hold, total holding cost is $8,400. That feels manageable and often gets ignored during analysis.

At six months, holding cost doubles to $16,800. That extra $8,400 comes directly out of profit.

At nine months, holding cost reaches $25,200. At this point, many deals that looked solid on paper are no longer worth the risk.

If the projected profit was $30,000, a six month delay wipes out more than half of it. A nine month delay nearly eliminates it entirely.

This is why time assumptions are not a detail. They are the deal. If your profit cannot survive delays, the deal was never as strong as it looked.

How Long Can You Hold Before the Deal Breaks?

Every real estate deal has a clock. You just do not see it until it is almost out of time.

The question is not whether holding costs exist. The real question is how long you can hold before the profit hits zero. That point is your break even holding period, and most investors never calculate it.

If you want to know how to calculate holding cost properly, this is where it actually matters.

What the Break Even Holding Period Really Means

The break even holding period is the maximum amount of time you can hold a property before holding costs consume all projected profit.

Once you pass that point, you are no longer taking risk for reward. You are taking risk for free.

This number gives you clarity. It tells you how much timeline flexibility you actually have, not how much you hope you have.

How to Calculate Maximum Hold Time Before Profit Hits Zero

The math is straightforward.

Take your projected profit and divide it by your monthly holding cost. The result is the maximum number of months you can hold before profit reaches zero.

If your expected profit is $24,000 and your monthly holding cost is $3,000, your break even holding period is eight months.

That does not mean you want to hold for eight months. It means that month nine turns the deal into a loss.

This calculation forces realism. It shows you whether delays are survivable or fatal.

Why This Matters for Flips, Refinances, and Rentals

On flips, thin margins disappear fast. If your break even period is short, pricing mistakes or slow sales can wipe you out.

On BRRRR deals, cash out refinances carry timing risk. Appraisal delays, seasoning requirements, or lender changes extend holding periods while interest continues to accrue.

On rentals, rent assumptions matter. If rents come in lower than expected or vacancy drags on, holding costs last longer than planned.

In every case, the break even holding period tells you how forgiving the deal really is. Strong deals survive delays. Weak deals demand perfection.

Holding Cost vs Carrying Cost in Real Estate

Holding cost and carrying cost are often used interchangeably in real estate, and in most practical situations, they mean the same thing. Both terms describe the ongoing expenses required to own a property over time.

Where confusion starts is in how formally the terms are defined versus how they are used in real world investing.

The Technical Difference Most Investors Do Not Need

Technically, carrying cost is the broader term. It can include any expense required to carry an asset over time, whether the property is stabilized or not. Holding cost is often used to describe those same expenses during a specific holding period, such as a flip, rehab, or vacancy.

In textbooks, that distinction matters. In real estate deals, it usually does not.

When investors talk about carrying costs, they are almost always referring to holding costs during a non income producing phase. Taxes, insurance, interest, utilities, and maintenance while time passes.

Why Investors Use the Terms Interchangeably

Real estate investing is practical, not academic. What matters is understanding how much time costs you, not which label you use.

Experienced investors focus on monthly burn rate and timeline risk. Whether someone calls it holding cost or carrying cost, they are talking about the same financial pressure.

If you understand how to calculate holding cost accurately and plan for delays, the terminology becomes irrelevant. The math is what protects you.

Knowing this distinction is less important than knowing how long your deal can survive.

How Smart Investors Protect Themselves From Holding Cost Risk

Experienced investors do not eliminate holding cost risk. They design deals that can survive it.

The difference between a beginner and a professional is not optimism. It is how much margin and flexibility is built into the deal before money is ever committed.

Conservative Timeline Buffers

Professionals assume delays before they happen.

Most experienced investors add a 25 to 50 percent buffer to their projected timeline. A three month rehab is underwritten as four to five months. A six month hold is modeled closer to eight or nine.

This is not pessimism. It is pattern recognition. Permits stall. Contractors get booked. Appraisals come in low. Markets slow unexpectedly.

Worst case planning keeps you solvent. Best case hope does not. If a deal only works when everything goes right, it is not a deal. It is a gamble.

Deal Filters That Eliminate Fragile Projects

Smart investors use filters to kill weak deals early.

Minimum margin rules ensure there is enough profit to absorb delays. Thin deals get passed on, even if they look exciting on paper.

Minimum cash on cash thresholds do the same thing for rental and BRRRR projects. If the numbers barely work in perfect conditions, they will not survive reality.

Filters protect your time and capital. They force discipline when emotions want to override math.

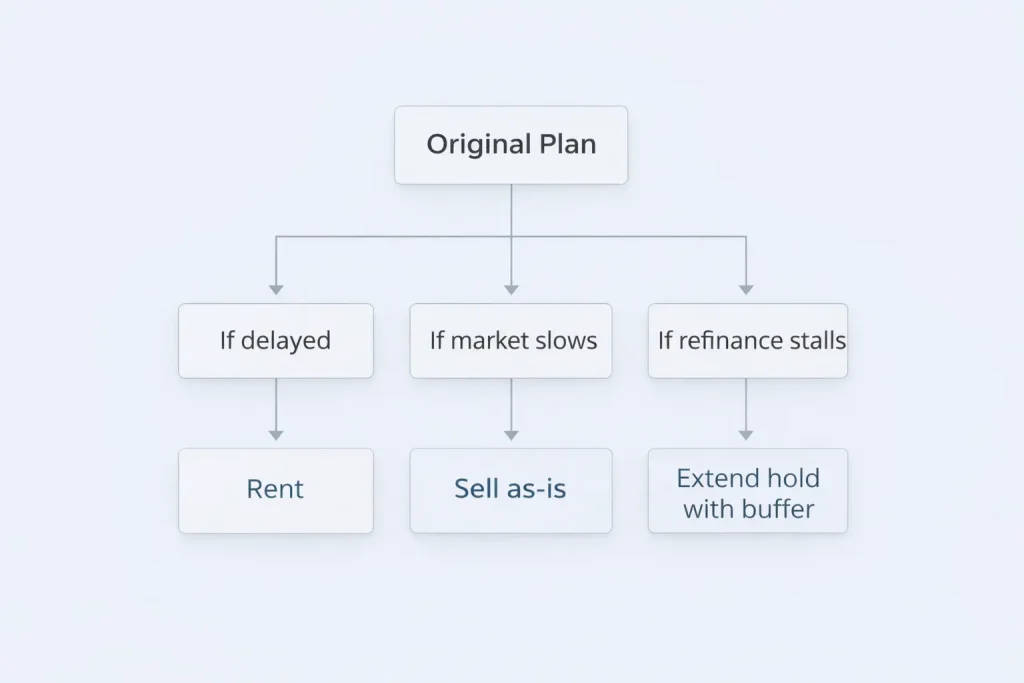

Exit Flexibility When Timelines Slip

Strong deals have more than one way out.

Plan B might be renting instead of flipping if the market slows. That only works if the holding costs are low enough to support temporary cash flow.

Plan C might be selling as is and preserving capital rather than forcing a bad finish. That option disappears quickly when holding costs run too high.

Flexibility is leverage. The more options you have, the less power time has over your deal.

Simple Holding Cost Checklist Before You Make an Offer

This is the checklist smart investors run before submitting an offer. It is not meant to be complicated. It is meant to expose weak deals quickly.

If you cannot answer these questions clearly, you are guessing. Guessing is how holding costs quietly win.

Pre Offer Holding Cost Checklist

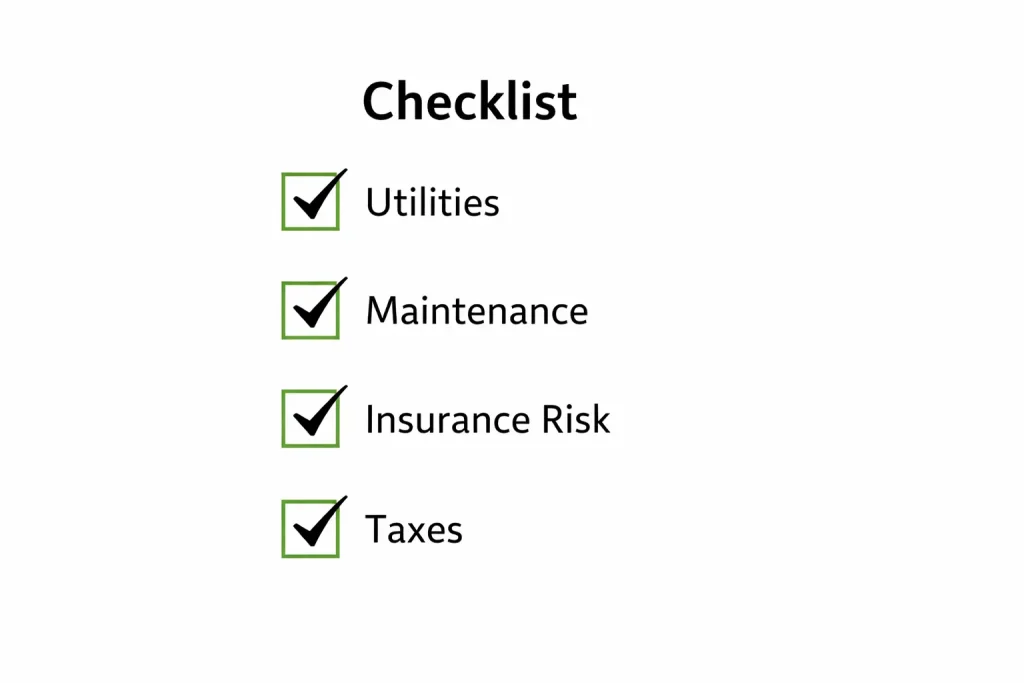

- Do I know my total monthly holding cost, not just the mortgage payment?

- Have I calculated holding costs using monthly numbers instead of annual estimates?

- Have I included financing interest, not just principal payments?

- Have I pro rated property taxes and accounted for potential reassessment after purchase?

- Am I using vacant property insurance or builder’s risk pricing instead of owner occupied rates?

- Have I included all utilities, including internet and trash?

- Have I budgeted for basic maintenance, lawn care, and code compliance during vacancy?

- Do HOA dues or special assessments apply, and are they verified?

- Have I included post renovation vacancy or lease up time in my timeline?

- Have I stress tested the deal with a timeline that is 25 to 50 percent longer than expected?

- Do I know my break even holding period in months?

- If this deal slips by one or two months, does it still make sense?

If the answer to any of these is no, the numbers are not finished yet.

A deal that survives this checklist is far more likely to survive real life.

The Deal Is Not the Price, It Is the Timeline

Most real estate deals do not fail because the purchase price was wrong. They fail because the timeline was unrealistic.

Holding cost is time multiplied by money. Every extra day you own a property without income increases the cost of the deal. That is why speed is not just an operational concern. It is a financial variable.

When investors focus only on price, they miss the risk that actually matters. Time is the multiplier that turns small monthly costs into large losses. The longer a property drags on, the more control the deal takes away from you.

This is why most bad deals do not look bad on day one. They look fine. Sometimes they even look great. The problem only shows up later, when holding costs quietly erase the margin you thought you had.

If you want deals that survive real life, underwrite time as aggressively as you underwrite price. That is where the real risk lives.