The Silent Profit Killer

Most real estate deals don’t fail because of purchase price. They fail because of time. That’s the part almost nobody models correctly, and it’s where carrying costs real estate investors underestimate the most quietly destroy returns.

On paper, a deal can look clean. The numbers pencil. The rehab budget feels reasonable. The exit looks obvious. But even with the right real estate investing tools to find deals and analyze numbers, time has a way of stretching when you least expect it. A permit stalls. A refinance drags. A tenant doesn’t move out on schedule. Nothing catastrophic happens, but every extra week adds pressure. And that pressure compounds.

Carrying costs rarely feel dangerous in isolation. A few hundred here. A payment there. Utilities running while the house sits empty. Insurance renewals you didn’t expect. Taxes that reset after purchase. None of these line items look fatal by themselves. The problem is that they stack, month after month, while your capital stays locked and your margin shrinks.

This is where many investors get blindsided. They underwrite best-case timelines and assume things will move on schedule. When they don’t, the deal doesn’t collapse immediately. It bleeds slowly. Cash flow tightens. Stress creeps in. Decisions get rushed. What started as a solid opportunity quietly turns fragile.

This post focuses on the carrying costs investors consistently miss or downplay. Not the obvious expenses everyone expects, but the hidden drains that only show up when time works against you. The goal is simple. Help you stress-test holding periods realistically, so delays don’t turn into expensive lessons you never planned for.

What Are Carrying Costs in Real Estate? A Quick Refresher

Plain-English Definition of Carrying Costs

Carrying costs in real estate are the expenses you pay simply to keep owning a property. They start the moment you close and continue for as long as you hold the asset. It does not matter whether the property is vacant, under renovation, or waiting on an exit. The costs still run.

If you own the property, you are carrying it. That’s the simplest way to think about it.

This is why carrying costs real estate investors underestimate are so dangerous. They feel passive and unavoidable, which makes them easy to ignore until they pile up. The longer a deal takes, the more these costs quietly compound in the background.

The takeaway here is simple. Carrying costs are not optional. They are time based obligations tied to ownership, not performance.

The Obvious Carrying Costs Investors Expect

Most investors correctly account for the obvious carrying costs. These are the expenses that show up clearly on statements and escrow breakdowns. Mortgage payments. Property taxes. Insurance. Utilities. HOA dues where applicable.

These costs feel controllable because they are predictable. You can estimate them with reasonable accuracy and plug them into a spreadsheet early. Because of that, they rarely feel threatening on their own.

The problem is not that investors forget these costs. The problem is that they assume these are the only carrying costs that matter.

When a deal underperforms, it’s almost never because these obvious expenses were misunderstood. It’s because something less visible went wrong.

The Hidden Carrying Costs Most Investors Underestimate

Hidden carrying costs show up through time, friction, and lost flexibility. They include delays, extended holding periods, financing drag, and opportunity cost. These costs are harder to model because they don’t arrive as a single bill.

A refinance that takes longer than expected. A flip that misses its selling window. A rental that stays vacant while repairs drag on. Each delay stretches the hold and amplifies every monthly expense already in place.

Opportunity cost is the most overlooked of all. While your capital is locked into one property, it cannot be used elsewhere. You lose optionality. You lose leverage. That loss rarely shows up in spreadsheets, but it absolutely affects long term returns.

The implication is critical. Hidden carrying costs are what turn good deals into fragile ones.

Why Carrying Costs Are Really a Clock

Carrying costs are not just expenses. They are a clock that starts ticking the day you take ownership. Every additional day the property is held increases risk and compresses margin.

When things go smoothly, the clock barely matters. When delays stack, it becomes the dominant variable in the deal. This is why time, not price, is the silent profit killer in real estate.

Once you understand carrying costs as a clock instead of a checklist, your underwriting changes. You stop asking whether the deal works on paper and start asking whether it survives delays.

That shift alone prevents more bad investments than almost any pricing strategy.

Why Investors Consistently Underestimate Carrying Costs

Optimism Bias in Deal Analysis

Most investors underestimate carrying costs because they start with optimism, not realism. The first version of a deal analysis usually reflects how the investor wants the project to go, not how projects typically go.

The numbers are not intentionally dishonest. They are just hopeful. Short timelines. Clean transitions. No friction. When you assume progress will be smooth, carrying costs feel small and manageable.

The issue is that optimism bias compresses time. When time is compressed, carrying costs look harmless. When time expands, those same costs become a problem very quickly.

The implication is subtle but important. The more confident an investor feels early, the less protection they build into the deal.

Best-Case Timelines Get Treated as Normal

Most projections are built around best-case scenarios. Rehab finishes on schedule. Permits are approved quickly. Appraisals come in clean. Financing moves without hiccups.

None of those assumptions are unreasonable on their own. The mistake is treating them as standard instead of optimistic.

When best-case timelines are baked into underwriting, there is no margin for delay. Every slip pushes the deal outside its original assumptions, even if nothing has gone terribly wrong.

This is how carrying costs real estate investors underestimate quietly take control. The deal did not fail. It just took longer than planned, and the model was never designed for that outcome.

Overconfidence in Rehab Schedules

Rehab timelines are one of the most common failure points. Investors assume contractors will show up on time, materials will arrive as expected, and scope will not change.

In reality, projects slow down for reasons that are hard to predict. Weather. Labor shortages. Inspection delays. Change orders. One small issue often creates a chain reaction.

Every extra week of rehab adds holding costs with no offsetting income. The property is not producing. It is only consuming cash.

The takeaway is simple. Rehab speed matters less than rehab resilience. If your deal only works when everything goes perfectly, it is already fragile.

Overconfidence in Refinance Timelines

Refinance delays are another blind spot. Many investors assume lenders will move quickly once the property is stabilized. In practice, underwriting, appraisals, and investor overlays can stretch timelines far beyond expectations.

Rate changes, guideline shifts, and appraisal issues can all slow the process. None of these feel dramatic in isolation, but they extend the holding period and magnify carrying costs.

The risk here is not just financial. It is psychological. Extended holds increase stress and reduce flexibility, which leads to rushed decisions later.

The implication is clear. Refinance timing should always be stress tested, not assumed.

Overconfidence in Lease-Up Speed

Lease-up is often treated as automatic. Clean unit equals quick tenant. That assumption breaks down fast in softer markets or seasonal slowdowns.

Vacancy during lease-up still carries full ownership costs. Utilities stay on. Insurance remains active. Taxes do not pause. Every vacant month extends the clock.

This is where investors realize that cash flow projections are only as good as the speed of stabilization. Delays here quietly eat returns without triggering obvious alarms.

The takeaway is that lease-up speed is a variable, not a guarantee.

The “It’ll Only Be a Few Months” Trap

This phrase shows up everywhere. A few months to finish rehab. A few months to refi. A few months to stabilize. Individually, each assumption feels reasonable.

Stacked together, they create exposure.

When multiple phases run slightly long, the total hold can double without any single disaster occurring. Carrying costs do not care why the delay happened. They only care that time passed.

The implication is uncomfortable but necessary. Deals rarely die from one big mistake. They bleed out through a series of small delays that were never modeled in the first place.

The Most Underestimated Carrying Costs Real Estate Investors Miss

Time Slippage Is the Number One Killer

Time slippage is the most underestimated carrying cost in real estate, and it causes more damage than any single expense line item. Every deal is modeled on a planned timeline, but very few follow it exactly.

Rehab delays happen when materials arrive late or scope expands. Permitting slows projects down in ways no contractor can control. Appraisals get pushed. Underwriting takes longer than expected. Contractors reshuffle schedules and your project drops in priority.

None of these issues feel dramatic on their own. The danger is cumulative. Each delay extends the hold, and every extended hold multiplies every other carrying cost already in place.

This is underestimated because investors model the timeline they intend to follow, not the timeline that typically happens. The clock does not care which one you planned for.

Vacancy Is a Monthly Burn Rate, Not a Temporary Phase

Vacancy is often treated as a short transition period instead of what it really is. A full monthly burn with no offsetting income.

Utilities stay on during vacancy. Lawn care and snow removal still happen. Security and monitoring become more important, not less. Power and water are often required for showings, inspections, or ongoing work.

Because vacancy feels temporary, investors mentally discount it. One empty month turns into two. Two turns into three. Carrying costs real estate investors underestimate quietly stack while they wait for stabilization.

The takeaway is simple. Vacancy should be modeled as a recurring expense, not a brief inconvenience.

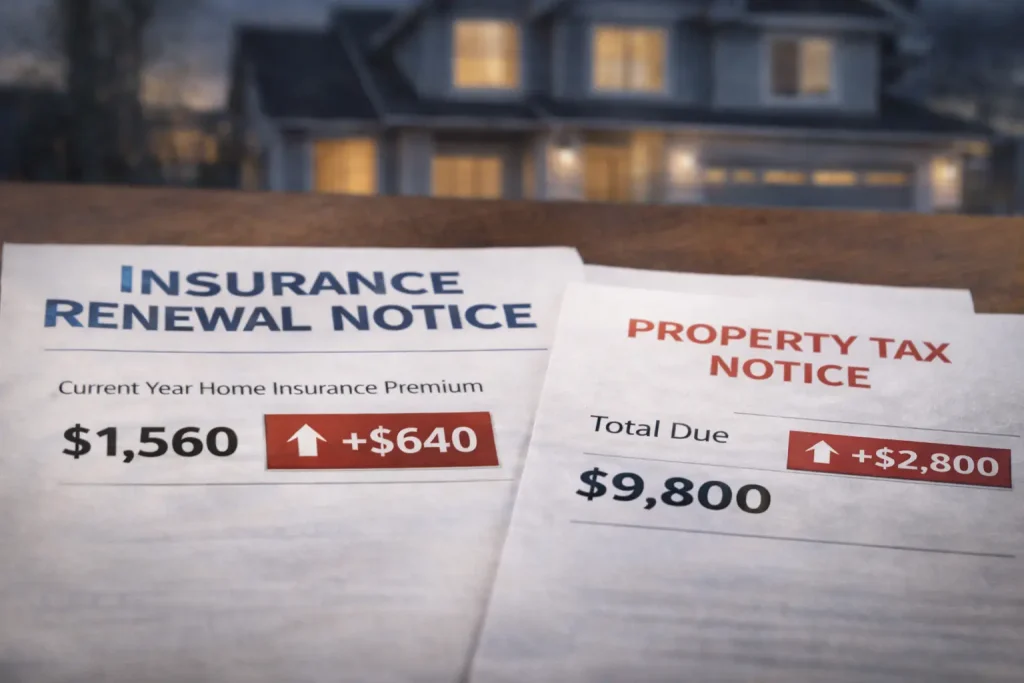

Insurance Costs Rise at the Worst Possible Time

Insurance increases hit hardest when a property is vacant or under renovation. Vacant property insurance premiums are higher by default. Builder’s risk policies add another layer of cost many investors gloss over.

What makes this dangerous is timing. Quotes are usually done early, before the true holding period is known. Mid project policy changes, renewals, or market wide premium hikes arrive later, when flexibility is already reduced.

Insurance rarely explodes overnight. It creeps up while the deal is already in motion. By the time the increase is noticed, the property has to be carried regardless.

The implication is that insurance is not a static number. It is a moving cost tied directly to time and risk.

Property Taxes Reset After Purchase, Not Before

One of the most common underwriting mistakes is using the seller’s tax bill. That number often has nothing to do with what the new owner will pay.

After purchase, reassessments can trigger sharp increases. Escrow shortages appear months later. Supplemental tax bills arrive long after closing. In some areas, tax increases lag just enough to surprise new owners who thought they were in the clear.

These increases do not show up immediately, which is why they are underestimated. By the time they hit, the deal has already absorbed months of carrying costs.

The lesson here is uncomfortable but necessary. If taxes reset upward, they do so permanently, not temporarily.

Interest Carry on Hard Money and Private Loans

Interest carry is one of the most aggressive forms of carrying cost. Interest only payments continue regardless of progress. Extension fees stack when timelines slip. Default penalties appear when expectations are missed.

Rate resets can occur if the hold stretches beyond original terms. Each extra month materially alters the deal’s return, especially on thin margin projects.

This cost is underestimated because investors focus on the purchase and exit numbers, not the time value of borrowed money in between.

The reality is simple. Hard money is not expensive because of rates alone. It is expensive because time is rarely predictable.

HOA Fees and Assessments Don’t Pause for Vacancies

HOA dues are owed whether the property is occupied or not. Monthly fees continue during vacancy, rehab, and listing periods.

Special assessments often arrive mid hold, not before purchase. Fines can be issued for exterior delays or incomplete work, adding pressure during already tight timelines.

HOAs are ignored because they feel fixed and manageable. Until they change. When they do, there is no negotiating leverage.

The implication is that HOA exposure should always be treated as variable, not guaranteed.

Maintenance Creep Slowly Becomes Urgent

Small maintenance issues compound over time. Deferred repairs turn into emergency fixes. Weather damage accelerates deterioration. Vacant properties attract vandalism and theft.

Investors often tell themselves they will handle these issues before selling or leasing. In practice, they fix the same problem twice. Once to stabilize, and again to make it presentable.

Maintenance creep is underestimated because it happens quietly. Each repair feels minor until the total starts to matter.

The takeaway is that holding longer increases wear, even when no one is living there.

Opportunity Cost Is the Carrying Cost No Spreadsheet Shows

Opportunity cost is the most invisible carrying cost and often the most painful. Cash tied up in one property cannot be deployed elsewhere. Flexibility disappears. Options shrink.

Missed deals never appear in reports, but they affect long term growth. Emotional pressure increases as sunk costs rise. Investors become committed not because the deal is strong, but because walking away feels worse.

This is the cost every investor feels but rarely calculates. Time spent stuck in one deal is time not spent building momentum elsewhere.

The implication is critical. Carrying costs are not just financial. They shape behavior, decisions, and risk tolerance in ways that compound over time.

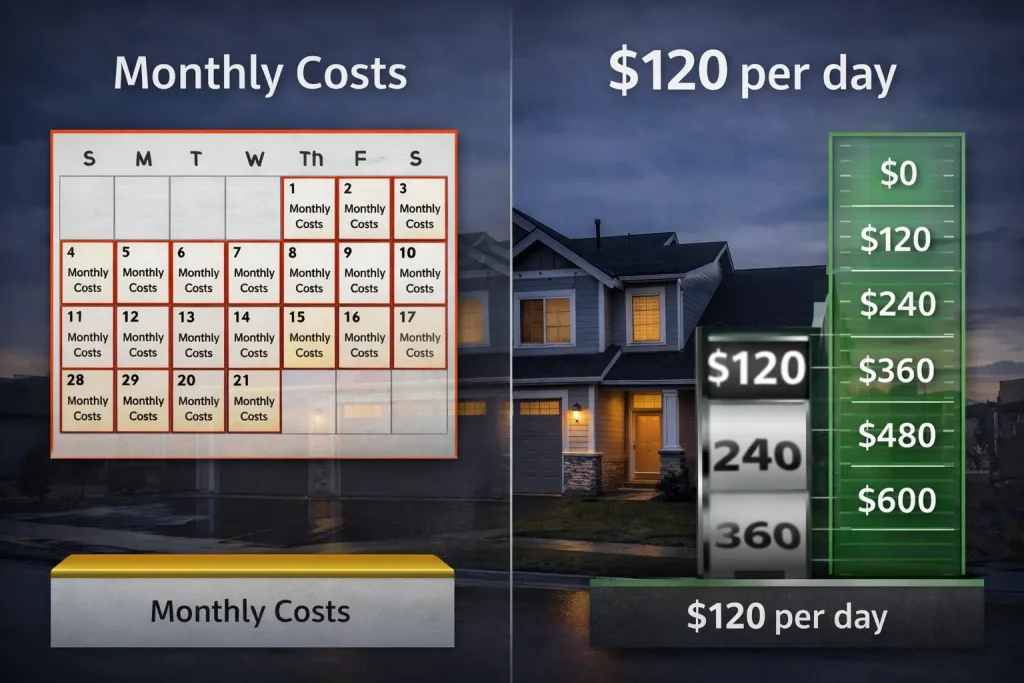

Monthly vs Daily Carrying Cost Reframes the Risk

Why Monthly Framing Hides the Real Cost

Most investors think about carrying costs on a monthly basis. A few thousand dollars a month feels manageable. It blends into the background with other expenses and stops feeling urgent.

That framing is deceptive.

When you think monthly, delays feel abstract. Another week does not register as a meaningful problem. Another inspection delay feels annoying, not expensive. Time stretches quietly without triggering action.

This is why carrying costs real estate investors underestimate keep compounding. Monthly framing smooths pain. It disguises urgency. It makes slow leaks feel harmless.

The implication is simple. Monthly thinking makes bad timing easier to tolerate.

Daily Carrying Cost Makes Time Impossible to Ignore

Daily framing changes behavior because it turns time into something tangible. Saying this property costs me one hundred twenty dollars a day to hold creates friction immediately.

Now delays feel expensive. A stalled permit is not just a delay. It is eight hundred dollars this week. A contractor reschedule is not an inconvenience. It is another thousand dollars gone by the end of next week.

Daily costs make the clock visible. Every day that passes has a price tag attached to it. That changes how investors prioritize follow ups, push vendors, and make decisions.

The takeaway is powerful. When time has a daily cost, urgency becomes rational instead of emotional.

How Daily Costs Change Decisions in Real Time

When investors shift to daily carrying cost thinking, behavior changes fast. Projects get managed tighter. Delays get escalated sooner. Marginal upgrades get questioned instead of approved automatically.

Daily framing also exposes weak deals earlier. If holding the property costs more per day than the deal can comfortably absorb, the problem becomes obvious before months pass.

This perspective forces a harder question. Is the deal strong enough to survive time working against it.

That question prevents more losses than better pricing ever will.

The implication is clear. If a deal cannot tolerate daily carrying costs, it was never as safe as it looked on paper.

Carrying Costs by Strategy Change the Risk Profile

Fix and Flip Deals Are Extremely Timeline Sensitive

Fix and flip deals are the most fragile when it comes to carrying costs. The margins are finite and the exit depends almost entirely on speed.

Every extra day adds mortgage interest, utilities, insurance, and taxes with no income to offset them. Rehab delays hit twice. Once through added labor and material costs, and again through extended holding time. Market slowdowns amplify this even further by stretching days on market after the work is done.

This is why carrying costs real estate investors underestimate hurt flippers the fastest. The deal can look profitable on paper and still collapse under time pressure.

The implication is simple. In fix and flip investing, time is not a secondary risk. It is the risk.

BRRR Strategies Break When Refinances Slip

BRRR deals live and die by the refinance. When it works smoothly, capital gets recycled and the deal scales. When it does not, carrying costs stack while cash stays trapped.

Refinance delays come from appraisals, seasoning requirements, lender overlays, or shifting guidelines. During that time, hard money or bridge loan interest continues. Taxes and insurance stay active. Vacancy may still exist if stabilization is incomplete.

The danger is that BRRR underwriting often assumes refinance timing as a certainty. When that certainty disappears, the entire strategy stalls.

The takeaway is critical. A BRRR that cannot survive a delayed refinance is not resilient. It is optimistic.

Buy and Hold Properties Are Riskiest in the Early Years

Buy and hold investments feel safer because they are long term. That perception hides where the real risk lives.

The early years carry the highest pressure. Debt service is highest. Reserves are usually lowest. Rents may not yet be optimized. Unexpected repairs hit before cash flow stabilizes.

If carrying costs spike early through tax reassessments, insurance increases, or vacancy, the deal feels stressful long before it feels profitable. Many investors underestimate this phase and overestimate how quickly stability arrives.

The implication is that long term safety does not eliminate short term risk. It concentrates it at the beginning.

Vacant Land Quietly Bleeds Cash

Vacant land has the simplest income profile. Zero. But the carrying costs still exist.

Property taxes continue. Insurance may still be required. Some parcels have HOA fees or maintenance obligations. There is no rent to offset any of it.

Because the expenses feel small individually, they are often ignored. Over time, that quiet bleed adds up without creating urgency.

This is one of the most underestimated carrying costs real estate investors face. Land does not scream when it loses money. It whispers.

The takeaway is straightforward. Zero income does not mean zero cost. It means every cost hits harder because nothing offsets it.

How to Stress Test Carrying Costs Correctly

Time Buffers Matter More Than Money Buffers

Most investors add contingency money and think they are protected. That helps, but it misses the real exposure. Time is what amplifies every cost.

Money buffers cover overruns. Time buffers protect survival.

If a deal runs long, every monthly expense repeats. Mortgage payments repeat. Interest repeats. Taxes repeat. Insurance repeats. A budget buffer gets used once. A time buffer absorbs pressure continuously.

This is why carrying costs real estate investors underestimate become dangerous. The spreadsheet assumes the hold ends on schedule. Real life does not.

The implication is simple. If you do not plan for time expanding, you are not stress testing. You are hoping.

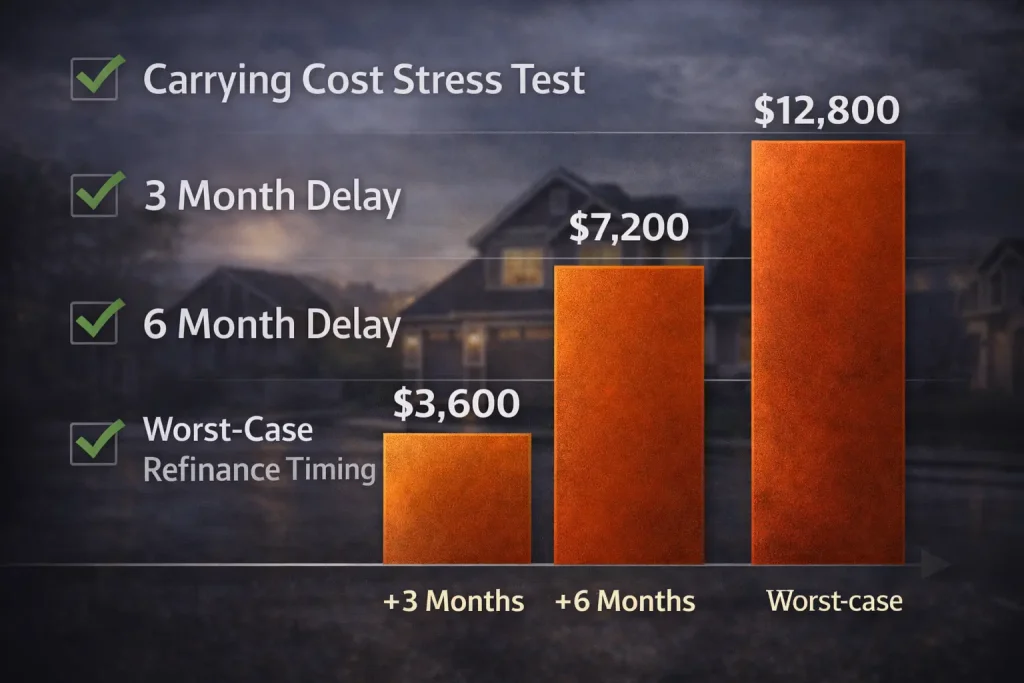

Model a Three Month Delay as the Baseline

A three month delay should be the starting point, not the worst case. This covers normal friction. Contractor slippage. Inspection delays. Appraisal timing. Minor lender issues.

If the deal becomes uncomfortable with just three extra months of holding, that discomfort is telling you something important. The margin is thinner than it looks.

This test is not about pessimism. It is about realism. Most projects experience at least some delay even when nothing goes wrong.

The takeaway here is clear. A deal that cannot tolerate three extra months is already fragile.

Model a Six Month Delay to Expose Weakness

A six month delay exposes structural weakness in the deal. This is where carrying costs start to dominate outcomes.

At this point, reserves get tested. Interest carry becomes noticeable. Taxes and insurance hit again. Vacancy becomes expensive instead of annoying.

Many investors skip this scenario because it feels extreme. In reality, it happens more often than people admit, especially when refinancing or selling into slower markets.

The implication is uncomfortable but necessary. If six extra months breaks the deal, you are relying on timing, not structure.

Stress Test the Worst Case Refinance Timing

Refinance assumptions deserve their own stress test. Appraisal issues. Seasoning requirements. Changing lender guidelines. Market shifts.

Ask how long the deal can survive if the refinance takes twice as long as expected. Or if rates move against you. Or if lender terms change mid process.

This is where many BRRR deals quietly fail. The property performs fine. The financing does not.

The takeaway is straightforward. Refinance timing should never be treated as guaranteed.

Ask Survival Questions Instead of Pencil Questions

Most investors ask whether a deal pencils. That is the wrong first question.

The better question is can I survive this if it goes slow.

Can you carry it for three more months without stress. Six more months without forcing bad decisions. A delayed refinance without panic.

When you frame deals this way, weak opportunities filter themselves out early. Strong ones stand out immediately.

The implication is powerful. Deals fail when survival was never part of the analysis.

Warning Signs Your Carrying Costs Are About to Explode

Escrow Shortages Are an Early Alarm

Escrow shortages are often the first sign that carrying costs are drifting higher than expected. Taxes or insurance increase, the lender recalculates payments, and the monthly obligation jumps.

This does not happen in isolation. When escrow goes negative, it usually means costs were underestimated earlier. The shortage shows up after the damage has already started.

Many investors treat this as a nuisance instead of a warning. That is a mistake. Escrow shortages indicate that the baseline cost of holding the property has permanently changed.

The implication is clear. When escrow adjusts upward, your margin just got thinner going forward, not just this month.

Extension Requests Signal Timeline Failure

Extension requests are a clear sign that the original timeline is breaking down. Whether they come from lenders, contractors, or sellers, extensions mean the deal is no longer following plan.

Each extension pushes the clock forward while every carrying cost keeps running. Interest accrues. Utilities stay on. Insurance remains active.

Extensions are often rationalized as minor. One more week. One more signature. One more inspection. In reality, they are compounding events.

The takeaway is simple. Extensions are not neutral. They are expensive.

Contractor Excuses Start Stacking

One excuse is normal. Weather delays happen. Material shortages happen. People get sick.

When excuses start stacking, the timeline is no longer under control. Missed days turn into missed weeks. Weeks turn into months.

At this point, carrying costs real estate investors underestimate begin to dominate the deal. The project is still moving, but not fast enough to justify the hold.

The implication is uncomfortable. When excuses multiply, time is slipping faster than progress.

Appraisal Issues Slow Everything Down

Appraisal problems rarely stop a deal outright. They slow it down.

Low values, reconsideration requests, or second appraisals add weeks or months to refinance or sale timelines. During that time, nothing changes operationally except one thing. You keep paying to hold the property.

Because appraisals feel external, investors underestimate their impact. They focus on the final number and ignore the time cost attached to resolving it.

The takeaway is straightforward. Appraisal delays are not just valuation problems. They are carrying cost problems.

Insurance Renewals Mid Project Add Pressure

Insurance renewals during a rehab or vacancy period often come with higher premiums or stricter terms. The property is still considered high risk, and the market may have shifted since the original quote.

This increase usually arrives when flexibility is lowest. The project is underway. The property cannot be sold easily. Coverage cannot be dropped.

Insurance changes mid project are rarely planned for. They quietly raise the burn rate without changing anything else.

The implication is critical. When insurance renews mid hold, carrying costs often reset upward with no easy way out.

The Carrying Cost Rule Smart Investors Actually Use

Stress the Timeline Before You Trust the Numbers

Smart investors assume time will work against them. Before trusting any projection, they ask a harder question. If this takes twice as long, does the deal still work.

This question forces realism. It removes best case thinking and replaces it with durability. If the answer is no, the deal is not broken. It is fragile.

Fragile deals depend on perfect execution. When anything slips, carrying costs real estate investors underestimate take over and squeeze the margin until there is nothing left.

The implication is simple. A deal that only works on schedule is not a strong deal.

Use Sleep Test Questions to Expose Risk

Another question experienced investors ask is less technical but more revealing. If I had to hold this for a year, could I sleep at night.

This is not about fear. It is about stress tolerance. Long holds increase mental load. Decisions feel heavier. Mistakes get costlier.

If the thought of an extended hold creates anxiety, that is useful information. It means the deal relies on timing rather than structure.

The takeaway is clear. Deals that cost you sleep usually cost you money later.

The Simple Carrying Cost Rule of Thumb

There is a simple rule smart investors use to filter weak deals early. If carrying costs exceed a meaningful percentage of total projected profit, the deal is fragile.

The exact percentage varies by strategy, but the concept stays the same. When holding costs consume too much of the upside, there is no buffer for delays.

At that point, time becomes the enemy. One slip can erase months of work.

The implication is powerful. Strong deals can absorb time. Fragile deals cannot.

Final Takeaway

Carrying costs are not just line items on a spreadsheet. They are time risk made visible. Every day you hold a property, you are exposed to compounding pressure that has nothing to do with how good the purchase price looked.

Most bad deals were not bad buys. They were bad holds. The numbers worked initially. The strategy made sense. What failed was the assumption that time would cooperate.

This is why carrying costs real estate investors underestimate matter so much. They do not announce themselves. They accumulate quietly while attention stays on the exit instead of the hold.

The investors who last the longest understand this. They do not win by projecting better scenarios. They win by building deals that survive delays, friction, and slow markets.

If a deal can withstand time working against it, everything else becomes easier.