Why the Best Distressed Deals Are Invisible

Most people searching for how to buy distressed properties assume the opportunity starts once a house looks cheap online. By the time a property is labeled distressed on Zillow, the leverage is usually gone. Either the margin has been competed away, or the deal was never real to begin with.

That is why so many buyers feel like they are doing everything right and still missing out.

The problem is not effort. It is where people are looking. Most buyers are trained to rely on listings, alerts, and surface level filters instead of understanding the systems that surface deals early. The investors who consistently buy well use real estate investing tools that help them identify pressure long before it becomes public, which is where real leverage actually forms.

This gap explains why cheap listings feel rare and competition feels constant. By the time something looks obvious, dozens of other buyers using the same tools and platforms have already seen it. Opportunity does not disappear. It just moves upstream into places most people never learn to look.

What “Distressed” Really Means (And What It Doesn’t)

Distress is not about how a property looks. It is about pressure. If you misunderstand this, you will spend your time chasing ugly houses instead of real opportunity. Once you separate financial stress from cosmetic issues, the entire strategy behind how to buy distressed properties becomes clearer.

Most buyers focus on damage. Experienced buyers focus on timelines.

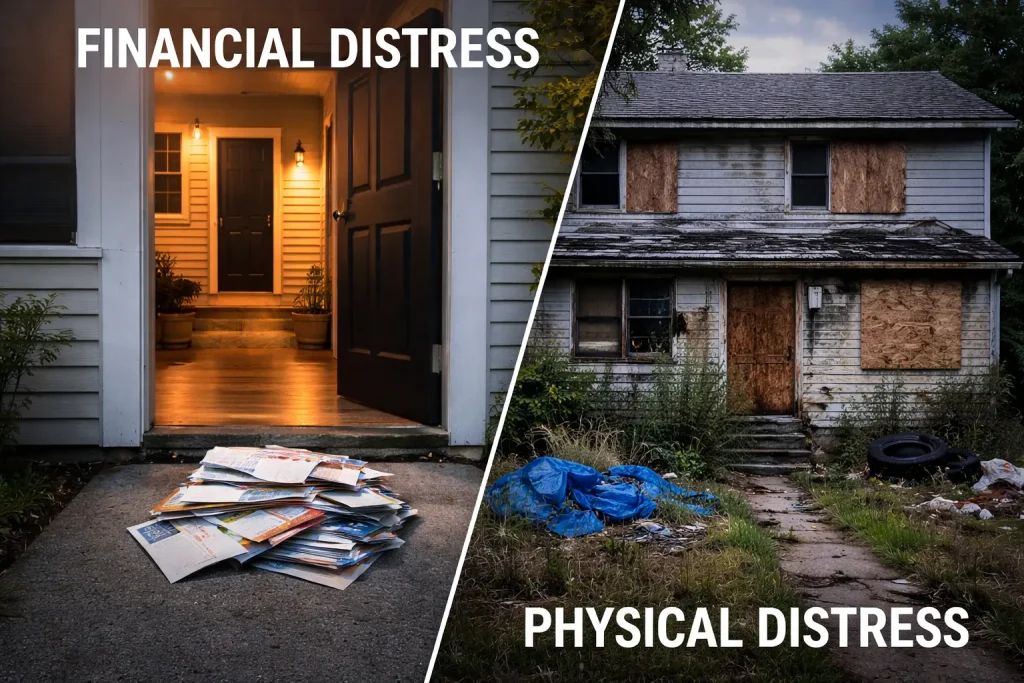

Financial Distress vs Physical Distress

Financial distress happens when the owner’s situation breaks down before the property does. Missed payments. Divorce. Job loss. Inherited property with no clear plan. These events create urgency long before a roof caves in or a kitchen gets gutted.

This kind of distress creates leverage because it compresses decision making. Sellers are not chasing top dollar. They are trying to solve a problem under time pressure. That is where clean offers win.

Physical distress is different. Deferred maintenance, outdated systems, or cosmetic neglect can look dramatic, but they do not always create urgency. Many owners sit on physically rough properties for years because there is no forcing function pushing them to act.

Catastrophic damage can actually work against you. Major structural issues shrink the buyer pool, complicate financing, and introduce uncertainty that kills otherwise solid deals. Ugly does not equal motivated.

The most profitable deals sit in the gap where the numbers still work but the owner’s situation does not.

The Five Common Distress Categories Buyers Confuse

Distress shows up in predictable buckets, even if the timing varies.

Pre foreclosure is early stage financial pressure. Payments are behind, but the clock has not run out yet. This is where leverage exists with minimal competition.

Foreclosure is late stage. Timelines are tight, rules are rigid, and buyers compete aggressively. Margins are thinner because everyone can see it.

REO or bank owned properties are already processed by institutions. The seller is no longer emotional, just procedural. Deals can exist, but creativity is limited.

Probate and estate sales introduce decision paralysis. Heirs want resolution, not projects. This creates opportunity when handled correctly.

Tax delinquency and municipal pressure quietly force action through fines, liens, or compliance notices. These sellers often act before the broader market notices.

The important takeaway is simple. Most profitable deals are financially distressed, not visually distressed. Once you stop hunting damage and start identifying pressure, the game changes.

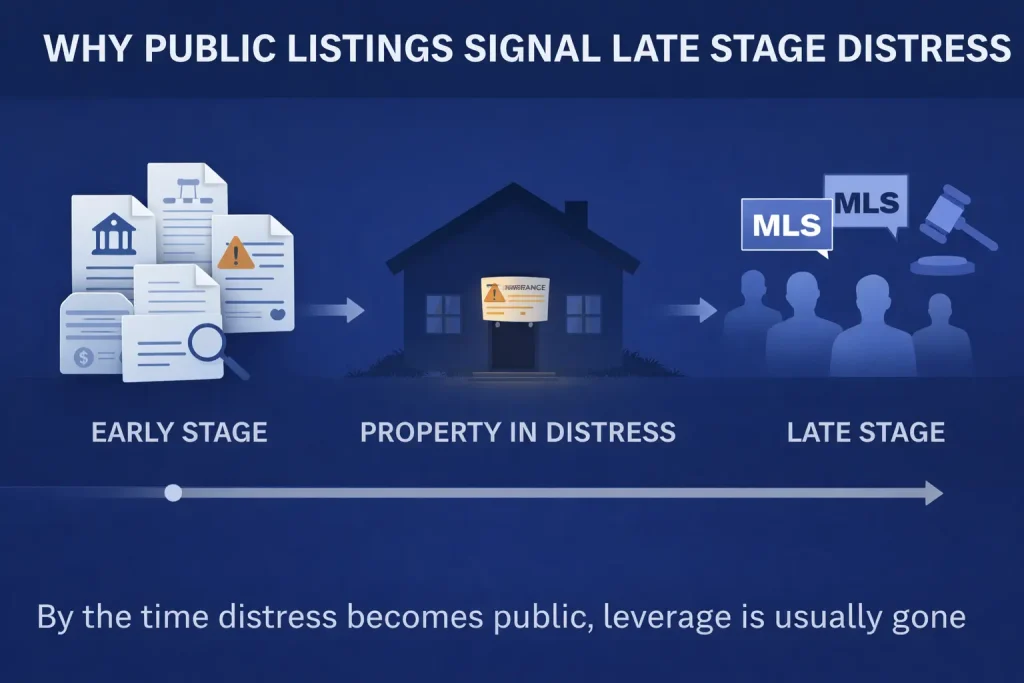

Why Most Investors Are Always Late

Most investors are not losing deals because they are slow or inexperienced. They are late because they rely on public signals to tell them when to act. By the time a property announces itself as distressed, the opportunity has already been diluted.

Distress is a process. Public visibility is the final step.

The Public Signal Trap

MLS tags, auction notices, and viral deal lists feel actionable because they are obvious. A property gets labeled as a foreclosure. A wholesaler blasts an email. A listing circulates on social media with the words needs work attached to it.

These signals trigger urgency, but they also trigger competition.

Once something becomes public, it is no longer scarce. Every investor with the same filters, alerts, and mailing lists sees it at the same time. Offers stack up. Terms tighten. Sellers gain leverage. Margins collapse quietly, even if the purchase price still looks low.

This is why so many deals look good on paper and disappoint in reality. The spread was competed away before you ever showed up.

How Competition Actually Finds Deals

Most investors assume competition is reacting faster than they are. That is rarely true.

Wholesalers are not fast. They are early. They operate upstream by talking to sellers before listings exist. By the time you see the deal, they have already extracted their margin.

Institutional buyers are not hunting Zillow. They buy from pipelines, data partnerships, and direct channels that never touch public platforms. Speed is irrelevant when access is exclusive.

Automated list scraping quietly feeds thousands of investors the same information at once. Everyone thinks they found something. No one did.

Competition is not about hustle. It is about positioning.

The key insight is simple. You do not beat competition with speed. You beat it with timing. When you learn to act before signals turn public, you stop chasing deals and start intercepting them.

Early Warning Signals Most People Miss

Distress does not appear overnight. It builds quietly, often months or years before a property ever hits the market. Buyers who understand how to buy distressed properties learn to recognize these early signals while others are still waiting for a listing notification.

The advantage comes from noticing pressure before it becomes visible.

Distress Signals That Appear Before Listings

Code violations and city notices are one of the earliest indicators. These are not cosmetic issues. They are deadlines. Fines, compliance orders, and inspection notices create financial and emotional pressure that most owners do not talk about publicly.

Utility shutoff patterns tell a similar story. Lapsed service, repeated disconnects, or long gaps in usage often signal vacancy, cash flow issues, or abandonment. These situations rarely resolve themselves.

Probate filings introduce uncertainty and delay. Heirs inherit property but not always the desire or ability to manage it. Decisions stall. Maintenance pauses. Pressure builds quietly.

Deferred maintenance can often be spotted through public records long before it is visible in photos. Permit gaps, outdated systems, or long stretches without improvements point to neglect that has not yet turned catastrophic.

Ownership duration mismatches are another overlooked signal. When a property has been owned far longer than surrounding homes, it often reflects aging owners, estate transitions, or resistance to change. Those situations eventually force decisions.

None of these show up as deals. They show up as tension.

Behavioral Red Flags That Signal Opportunity

Behavior often matters more than paperwork.

Absentee owners tend to delay decisions because the property is not part of their daily life. Distance creates avoidance, not urgency, until something forces action.

Inherited property indecision is common. Multiple decision makers. Emotional attachment. No clear plan. This paralysis often lasts until external pressure breaks the stalemate.

The most important distinction is emotional paralysis versus urgency. Sellers stuck in paralysis will talk without acting. Urgent sellers move quickly once a path appears.

Learning to spot this difference changes everything. Early warning signals are not about finding deals. They are about finding moments before deals exist.

Where to Find Distressed Properties Before They Hit the Market

If you are serious about how to buy distressed properties early, you have to stop relying on listing platforms to surface opportunity. The best deals are found upstream, in places most buyers never look and would not know how to interpret even if they did.

This is where leverage actually comes from.

Off Market Sources That Actually Work

County records are one of the most consistent sources of early stage distress. Probate filings, liens, and tax delinquencies all indicate pressure without publicity. These records do not mean a property is for sale. They mean a decision is coming.

Code enforcement databases are another overlooked source. Violation notices create deadlines, fines, and compliance stress. Owners often try to ignore them until the situation escalates. That window is where early conversations happen.

Eviction filings reveal more than tenant issues. They often signal cash flow problems, management fatigue, or owners exiting a bad situation. Many landlords decide to sell quietly once they realize the problem is not temporary.

HOA violation notices create a unique kind of pressure. Fines accumulate. Rules tighten. Owners who do not want conflict often choose resolution over resistance.

Local courthouse patterns matter more than individual filings. When you track activity over time, you start to see which situations resolve and which ones spiral. That pattern recognition becomes a competitive advantage.

These sources do not hand you deals. They give you timing.

Why the MLS Is a Lagging Indicator

The MLS is not useless. It is just misunderstood.

It works well for context. You can validate pricing, study comparables, and understand market velocity. It tells you what finished deals look like, not where they started.

What it cannot do is create leverage. Once a property hits the MLS, the seller has already chosen exposure over discretion. That choice invites competition and resets negotiating power.

Think of the MLS as a rearview mirror. It shows you what already happened. If your goal is to buy before others notice, your work has to happen before a listing ever exists.

How to Analyze a Distressed Property Without Lying to Yourself

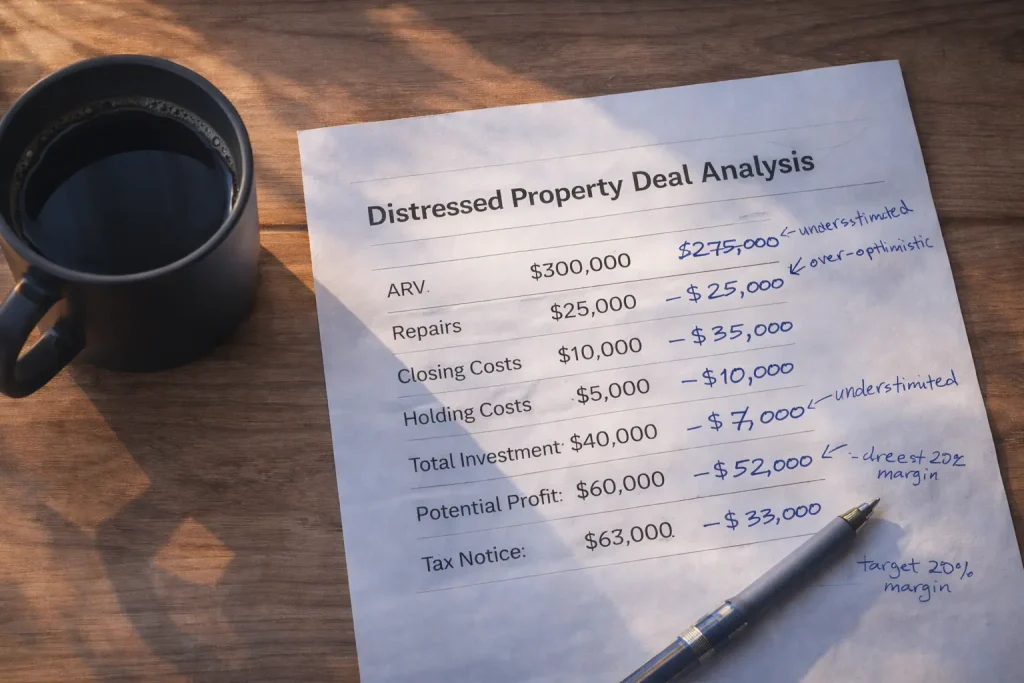

Most people do not lose money on distressed properties because they cannot find deals. They lose money because they convince themselves a deal works when it does not. Learning how to buy distressed properties responsibly means building analysis that resists optimism instead of rewarding it.

The numbers have to survive reality, not spreadsheets.

Estimating ARV Without Optimism Bias

ARV is where most self inflicted damage happens. Buyers anchor to the highest comp, not the most likely outcome. They assume perfect execution in imperfect markets.

Conservative comp selection fixes this. Look for recent sales that match the property as it will realistically exist, not as you hope it will. Same size. Same layout. Same neighborhood. Ignore outliers that required exceptional conditions to sell.

Market velocity matters just as much as price. How long are renovated homes actually sitting before selling. A strong ARV in a slow market behaves very differently than the same number in a fast one.

If the exit depends on best case pricing, it is not an exit. It is a gamble.

Repair Cost Reality Check

Novice estimates are almost always wrong because they focus on visible problems. Floors. Paint. Kitchens. What hurts budgets lives behind walls and underground.

Older systems fail in clusters. HVAC exposes electrical. Plumbing reveals structural rot. Permits uncover code requirements no one budgeted for. Each discovery compounds cost and time.

Contingency buffers are not pessimism. They are equity protection. If your deal does not work with a meaningful buffer, it does not work at all.

Experienced buyers do not ask how cheap repairs can be. They ask how expensive they could realistically become.

The Real Cost of Cheap

Cheap properties carry invisible expenses that do not show up at closing.

Holding costs eat quietly. Taxes, insurance, utilities, financing, and maintenance stack every month the project drags on. Time risk compounds when markets slow or contractors miss deadlines.

There is also emotional bandwidth. Stress, decision fatigue, and constant problem solving drain focus from better opportunities. Many buyers underestimate how much attention a distressed property demands.

Cheap prices feel good. Expensive time does not. The goal is not to buy cheaply. It is to buy cleanly and exit predictably.

Financing Distressed Deals Before Others Can

Financing is where most early stage distressed deals die. Not because they are bad deals, but because the buyer cannot execute fast enough. Understanding how to buy distressed properties early means aligning your financing with the reality of distress, not the rules of retail lending.

Speed and certainty matter more than rate.

Why Traditional Financing Fails Early Stage Distress

Traditional loans are built for clean properties and stable situations. Early stage distress is neither.

Appraisal limitations are the first choke point. Appraisers value based on current condition and recent sales, not future potential. Distressed properties often appraise below contract price even when the deal makes sense long term.

Habitability requirements create another barrier. Missing flooring, exposed wiring, roof issues, or non functioning systems can kill loan approval instantly. Lenders are not evaluating upside. They are minimizing risk.

The result is predictable. Deals stall. Deadlines get missed. Sellers lose confidence. The opportunity disappears.

This is why buyers relying on traditional financing are almost always late.

Financing Options That Move Faster

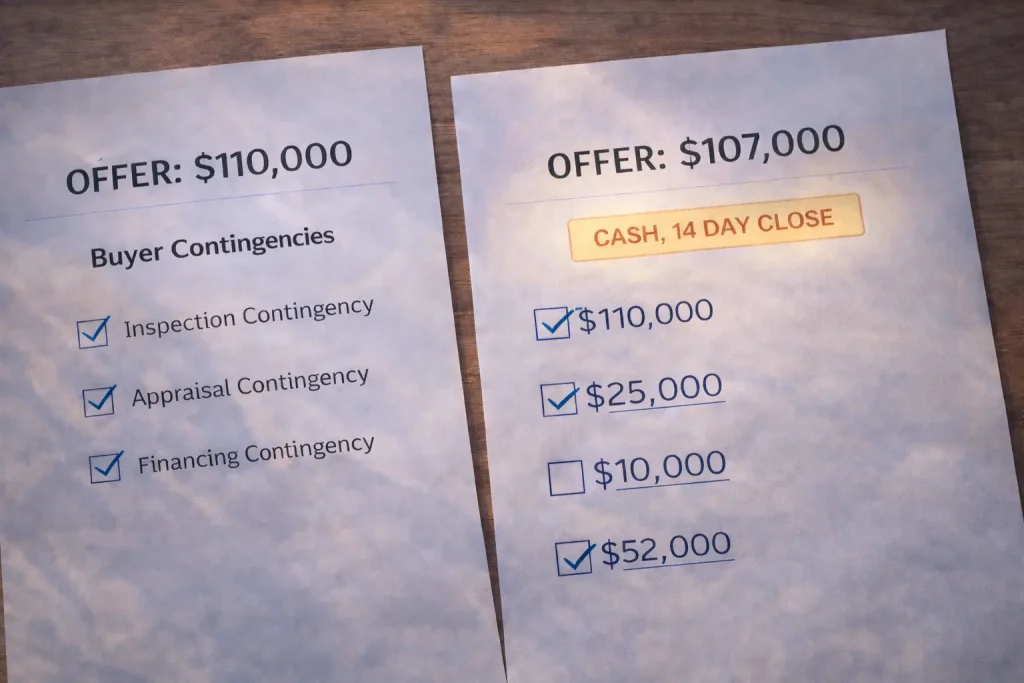

Cash is the cleanest option. No appraisal. No underwriting delays. Sellers value certainty more than price when timelines are tight. Cash removes friction and builds leverage immediately.

Hard money works when used intentionally. It is expensive, but it buys speed. When the spread is real and the exit is clear, hard money can unlock deals traditional lenders will never touch.

Private lenders sit between cash and institutions. These relationships are built on trust, not checklists. Terms vary, but flexibility is the advantage.

Creative structures like subject to or seller financing can work in specific situations, but they require experience and clean execution. These tools solve problems. They are not shortcuts.

The rule is simple. Speed plus certainty beats the highest offer. When sellers feel confident you can close, price becomes secondary.

Hidden Risks That Kill First Time Investors

Most first time investors do not fail because they miss opportunity. They fail because they underestimate risk. Understanding how to buy distressed properties safely means knowing where deals quietly fall apart after the contract is signed.

The biggest threats are rarely obvious at first glance.

Legal and Title Risks

Liens are one of the fastest ways to turn a good deal into a bad one. Tax liens, mechanic liens, and municipal fines can survive ownership transfers if not handled correctly. Many buyers assume the closing process automatically fixes this. It does not.

Unreleased judgments create similar problems. Old lawsuits, unpaid obligations, or improperly cleared records can delay or block resale. These issues often surface late, when timelines are tight and options are limited.

Occupancy issues are another silent killer. Buying a property with tenants, former owners, or unknown occupants introduces legal processes that move far slower than your financing clock. Evictions take time, money, and emotional energy.

If you do not control possession, you do not control the deal.

Operational Risks Most Beginners Miss

Contractor dependency is one of the most underestimated risks. When timelines rely on a single person or crew, delays compound fast. One missed week turns into a missed month.

Permit surprises add friction where none was expected. Work that seems minor can trigger inspections, code upgrades, and additional costs that were never part of the original plan.

Scope creep quietly destroys margins. Small changes feel reasonable in isolation. Together, they erase profit. Most projects fail not from one big mistake, but from many small ones.

Execution matters more than vision.

Psychological Traps That Override Logic

Overconfidence shows up when early wins or good spreadsheets create false certainty. Distressed deals punish assumptions.

The sunk cost fallacy keeps buyers moving forward because they already invested time, money, or ego. Walking away feels like failure, even when it is the right move.

The most dangerous thought is this deal has to work. Once that mindset takes hold, numbers get adjusted, risks get minimized, and warning signs get ignored.

Successful investors stay detached. Deals are options, not obligations.

Why Distressed Properties Are an Equity Strategy, Not a Hack

Distressed properties are not a trick or a shortcut. They are a mechanism for creating equity when the market will not give it to you. Once you understand how to buy distressed properties this way, the strategy stops being transactional and starts becoming structural.

This is about ownership, not wins.

Distress as Forced Equity Creation

Forced equity comes from solving a problem, not guessing direction. Distress creates mispricing because sellers value relief more than optimization. When you remove pressure, you are paid in equity.

This equity is created at purchase, not hoped for later. It exists regardless of appreciation or rate changes. That is why distress works even in flat or uncertain markets.

Buyers who rely on appreciation need timing and luck. Buyers who create equity control outcomes.

Why This Works Best for Long Term Owners

Long term owners benefit most because they are not forced to exit on a schedule. They can refinance, rent, or hold through volatility. Distress gives them margin of safety that short term strategies often lack.

This approach also absorbs mistakes better. When equity exists on day one, small errors do not destroy the deal. They get diluted over time.

Short term thinking demands perfection. Long term ownership rewards structure.

How This Compounds Over Multiple Cycles

Each distressed acquisition strengthens the next one. Equity becomes capital. Capital becomes access. Access creates better timing and better terms.

Over multiple cycles, this compounds quietly. Not through leverage stacking, but through position improvement. Better financing. Better networks. Earlier entry points.

This is not a hack. It is a system that rewards patience, discipline, and consistency.

A Simple Framework for Buying Before Others Notice

Buying early does not require complex tactics. It requires a repeatable process that prioritizes timing over volume. When people ask how to buy distressed properties before competition shows up, this is the framework that matters.

Simple systems beat clever strategies.

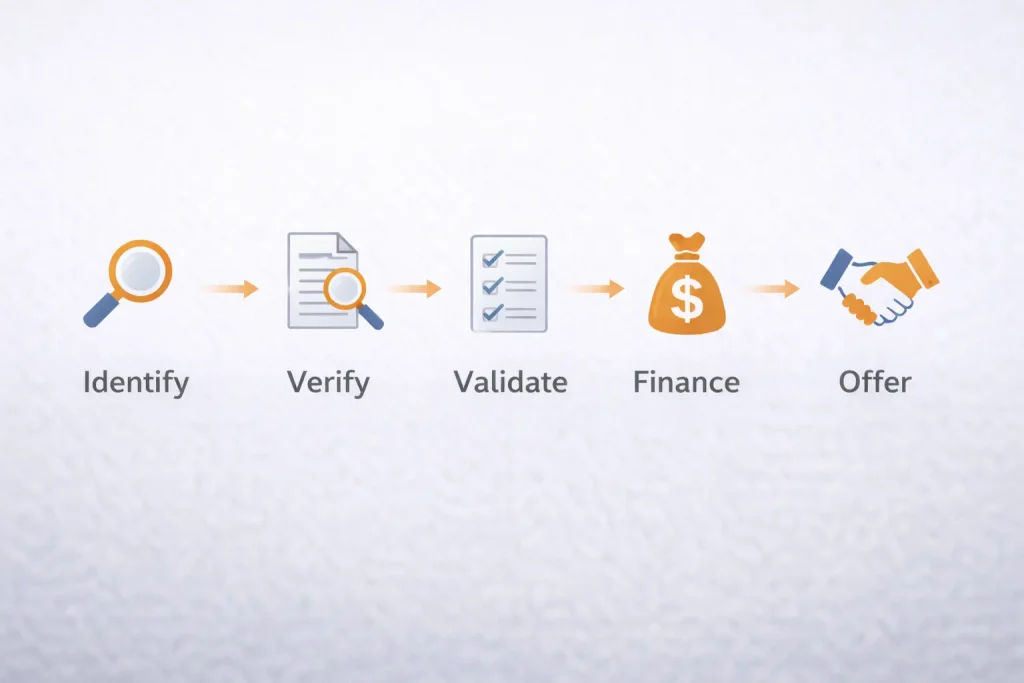

Step by Step Early Distress System

The first step is identifying distress signals, not listings. Public listings are outcomes. Signals are inputs. Code violations, legal filings, unpaid taxes, ownership transitions. These tell you a decision is coming even if the seller has not admitted it yet.

Next, verify timeline pressure. Not every distressed situation is actionable. The presence of a deadline is what creates leverage. Fines, court dates, compliance windows, or personal timelines turn curiosity into urgency.

Then validate numbers conservatively. Assume delays. Assume overruns. Assume slower exits. If the deal only works when everything goes right, it does not work.

Secure fast financing before you need it. Sellers sense uncertainty immediately. Confidence comes from preparation, not promises.

Finally, make simple, clean offers. Few contingencies. Clear timelines. No drama. The goal is not to impress. It is to reduce friction.

This framework works because it respects how distress actually unfolds. You are not racing other buyers. You are arriving before they know there is a race.

Who Should (and Shouldn’t) Buy Distressed Properties

Distressed properties are not universally good or bad. They are situational. Whether they work depends less on intelligence or ambition and more on temperament and structure. Knowing how to buy distressed properties also means knowing when you should not.

Fit matters more than strategy.

Who Distressed Properties Are a Good Fit For

Buyers comfortable with uncertainty tend to do well here. Distress rarely comes with complete information. There are gaps, unknowns, and moving parts. If you need certainty before acting, this space will feel uncomfortable.

Investors who prioritize equity over convenience are another strong fit. Distressed deals trade ease for margin. The reward comes from solving problems others avoid, not from frictionless transactions.

Operators who value systems outperform consistently. When decisions are guided by checklists, timelines, and conservative assumptions, emotion stays out of the way. Distress rewards process, not instinct.

These buyers are not fearless. They are prepared.

Who Distressed Properties Are a Bad Fit For

Timeline sensitive buyers struggle here. If you need a guaranteed closing date or a predictable move in window, distress will test your patience and your finances.

Emotion driven decision makers get hurt quickly. Distressed situations trigger empathy, urgency, and attachment. When feelings override structure, bad decisions follow.

Anyone relying on perfect information should avoid this space entirely. Distress never arrives fully packaged. Waiting for clarity usually means waiting until the opportunity is gone.

Knowing your limits is a strength, not a weakness.

What This All Really Comes Down To

Distressed properties reward those who see early and act clean. Not louder. Not faster. Cleaner.

The real edge is not effort. It is awareness and positioning. When you understand where pressure forms and prepare before others react, the market stops feeling crowded.

Opportunity does not disappear. It just moves upstream.