Estimated Max HELOC Line

$0

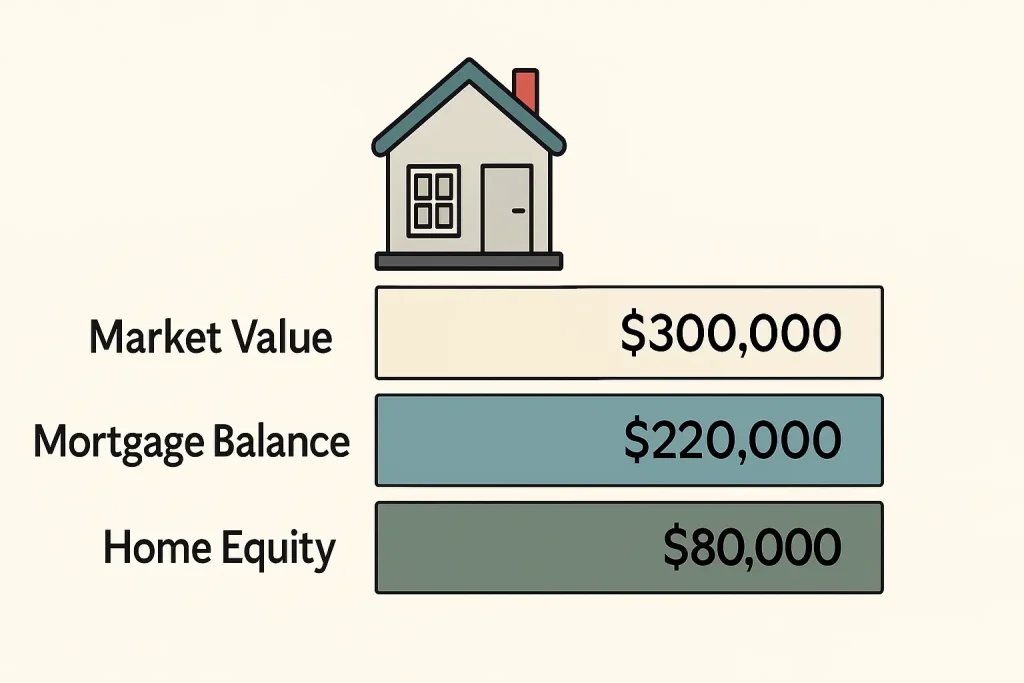

Based on home value, mortgage balance, and CLTV limit.

Monthly Payment During Draw

$0/mo

for 0 years (interest-only)

Monthly Payment After Draw

$0/mo

for 0 years (fully amortizing)

How to Use This HELOC Calculator

You don’t need to be a loan officer or a math whiz to figure out how much home equity you can borrow. That’s exactly why I built this free HELOC calculator to help homeowners cut through the jargon and get straight to the numbers. If you want the bigger picture of how home equity can backfire, this post breaks it down simply.

Here’s how to use the calculator:

1. Enter your home’s estimated value.

You can pull this from a recent appraisal, your county property records, or even a quick Zillow estimate. The more accurate your number, the closer your results will be to what a lender might offer.

2. Add your current mortgage balance.

This tells the calculator how much equity you’ve built up so far. The less you owe, the more borrowing power you’ll have.

3. Adjust your desired loan-to-value (LTV) ratio.

Most lenders let you borrow up to 80–90% of your home’s value (including your existing mortgage). This field helps you see your maximum potential credit line based on that percentage.

For example, if your home is worth $450,000 and you owe $300,000, an 80% LTV means you could access roughly $60,000 in available credit.

4. Enter your planned HELOC draw amount.

This is how much you actually plan to use from your line of credit, not necessarily the full amount you qualify for. You can play around with this number to see how your monthly payments change.

5. Set your interest rate and time frames.

Interest Rate (APR%) – Try different rates to see how your monthly payment changes. HELOCs often use variable rates that move with the market.

Draw Period (Years) – This is the time you can borrow, repay, and borrow again (commonly 10 years).

Repayment Period (Years) – Once the draw period ends, you’ll start repaying the balance with fixed monthly payments over this term.

6. Hit “Calculate.”

You’ll instantly see three key numbers:

- Your estimated maximum HELOC line

- Your monthly payment during the draw period (usually interest-only), and

- Your monthly payment after the draw period (when full repayment begins).

These are realistic ballpark figures to help you plan before you talk to a lender.