Most people think of their home as a place to live. A roof, a few walls, maybe a fenced backyard for the dog. But what they often miss is that it’s also a financial engine sitting quietly in the background, growing in value while they sleep.

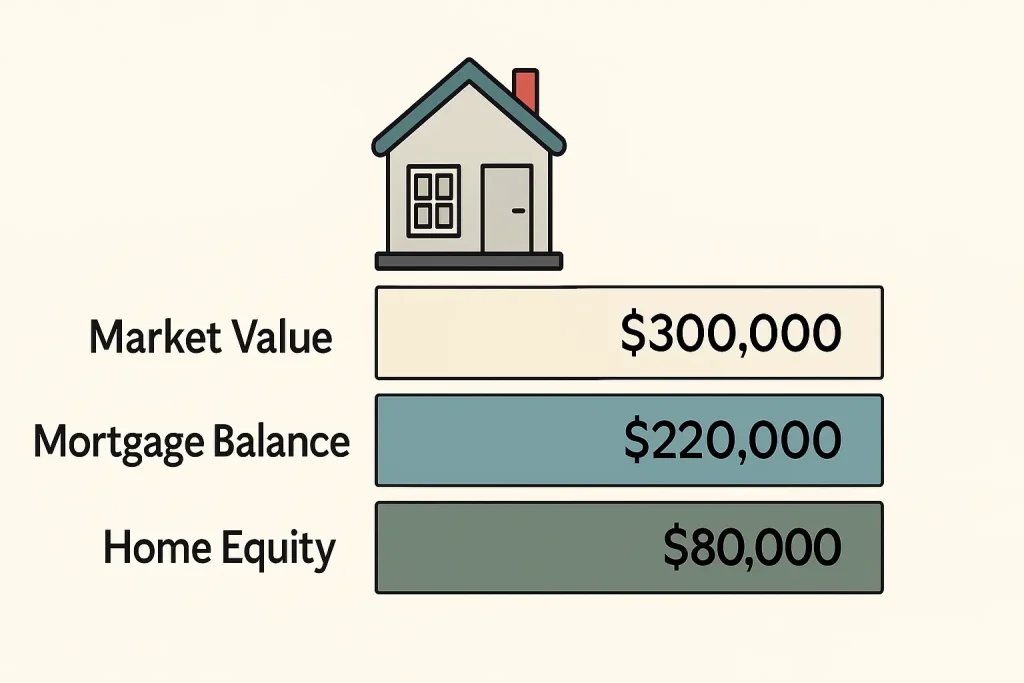

Home equity is simple. It’s the difference between what your home is worth and what you still owe on your mortgage. If your house is worth $400,000 and you owe $260,000, you’ve got $140,000 in equity. That’s your ownership slice—the part that actually belongs to you.

The beauty of home equity is that it grows without you doing much. Every mortgage payment chips away at your loan balance, building equity through principal paydown. At the same time, market appreciation does the heavy lifting in the background. According to the Federal Reserve, U.S. home values have consistently climbed over the long run, helping homeowners build substantial net worth over time.

But here’s the catch, most people never use it. They let their equity sit there, doing nothing. Dead money locked in drywall. And while that might feel “safe,” it’s also the reason many homeowners never move beyond being house-rich and cash-poor. The wealthy see home equity differently. They treat it like a tool, not a trophy. Something that can be tapped strategically to build more wealth, create passive income, or accelerate financial independence.

And before you think this is risky business, know that equity use isn’t about reckless borrowing. It’s about learning to manage leverage the same way investors do—measured, calculated, and backed by real numbers. When done right, your home equity isn’t just a nest egg. It’s your hidden wealth engine.

For more perspective on how homeowners are using equity to grow long-term wealth, the Consumer Financial Protection Bureau offers clear insights into the benefits and responsibilities that come with tapping into it responsibly.

The 3 Safe Ways to Tap Home Equity

Before you use your home equity, you need to understand the tools. Not all equity loans are created equal. Some give you flexibility, others give you predictability, and a few can completely reset your mortgage. The trick is knowing which one fits your goals—and your risk tolerance.

1. Home Equity Line of Credit (HELOC)

A HELOC is like a credit card backed by your house. You get a revolving line of credit you can draw from whenever you need it—perfect for projects that don’t require all the cash up front.

Most lenders give you a 10-year draw period where you can borrow, repay, and borrow again as needed. During this time, you’ll usually make interest-only payments, which keeps your monthly costs low. After that, the repayment phase begins, and you start paying both principal and interest.

HELOCs are great for homeowners who want flexibility. Maybe you’re renovating your kitchen one month and adding a deck the next. Or maybe you want to fund small real estate investments that generate fast returns. The key benefit is control—you only pay interest on what you actually use.

For more background, the Consumer Financial Protection Bureau explains exactly how HELOCs work and what to look out for before applying.

2. Home Equity Loan

A home equity loan is more like a traditional loan than a revolving credit line. You get a fixed lump sum upfront, a fixed interest rate, and a set repayment schedule—usually 5 to 20 years.

Because the payments are the same every month, this option is ideal for people who value predictability or need funds for a single, large project. Common uses include debt consolidation, major renovations, or financing a high-return investment where you know the total cost upfront.

Think of it as “borrowing once, paying once.” No surprises, no fluctuating interest rates. Just straightforward financing that’s easy to budget around.

For a clear explanation of how these loans differ from lines of credit, the Federal Trade Commission offers a solid overview of home equity loan terms and consumer protections.

3. Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a new, larger one—and you pocket the difference in cash. This method often works best when mortgage rates are lower than your current rate or when you need to access a substantial amount of equity all at once.

For example, if your current mortgage is $250,000 and your home is worth $450,000, you might refinance into a $350,000 loan. You pay off your old mortgage and walk away with $100,000 cash (minus closing costs).

Homeowners often use this method to buy investment property, fund major upgrades, or consolidate high-interest debt into one lower-rate payment. According to Bankrate, a cash-out refinance can be a smart move when the money is used to improve your financial position, like paying off high-interest credit cards or boosting your home’s value through renovations. The advantage is that you get long-term, fixed-rate stability, but the trade-off is resetting your mortgage clock and increasing your overall loan balance.

How to Use Home Equity to Actually Build Wealth

Accessing your home equity is one thing. Using it strategically is what separates homeowners who stay stuck from those who build real wealth. Your equity can either sit quietly inside your walls doing nothing, or it can go to work generating income, increasing your net worth, and speeding up your financial goals.

1. Invest in Cash-Flowing Real Estate

This is the classic wealth play. You pull $100,000 of equity from your primary home, use it as a down payment on a small duplex, and suddenly you’ve got two tenants paying off that new property while you collect $600 in positive cash flow each month.

You’re building wealth in three ways: monthly income, property appreciation, and long-term tax benefits. The IRS allows you to deduct mortgage interest, depreciation, and certain expenses related to rental property ownership (irs.gov). The key is running your numbers before you borrow. Make sure the return on your new investment comfortably exceeds the cost of borrowing from your home.

2. Eliminate High-Interest Debt

Using home equity to wipe out 22% credit card debt and replace it with an 8% HELOC can completely change your monthly cash flow. That freed-up money can then be redirected into investments, savings, or even paying down your mortgage faster.

But this only works if you stay disciplined. The trap most people fall into is paying off their cards, feeling relief, then running them back up again. That’s how you turn a smart move into a disaster. The goal isn’t just debt relief, it’s permanent cash flow recovery. Once the balances are gone, redirect the old payment amounts toward assets that grow instead of liabilities that drain.

3. Fund Value-Boosting Renovations

Not all upgrades are created equal. Some add comfort, others add value. If you’re strategic, a renovation can immediately increase your home’s appraised value and expand your equity cushion.

According to Remodeling Magazine’s 2024 Cost vs. Value report, kitchen and bathroom remodels typically recoup between 70% and 80% of their cost at resale. That means if you spend $30,000 upgrading a kitchen, you could see roughly $21,000–$24,000 reflected in higher market value—plus a more functional home to enjoy in the meantime.

Renovations are especially powerful when you’re looking to refinance or sell in the next few years. They can raise your appraisal enough to help you qualify for better loan terms or eliminate PMI faster.

4. Start or Expand a Business (Advanced Strategy)

This one’s not for everyone—but if you’ve got experience or a proven business model, using a portion of your home equity to launch or scale can be a game-changer.

Take a real-world example: tapping $50,000 of equity to start a small rental management company. That capital can cover startup costs, marketing, and early staffing—turning a dormant asset into an income-producing venture.

The risk, of course, is that your home is tied to the loan. So you need to treat it like an investment pitch. Run your numbers. Make sure your expected ROI far exceeds the interest rate on your equity loan. Most small business advisors suggest you don’t bet the house—literally—on an untested idea. The U.S. Small Business Administration has excellent guidelines for evaluating this kind of financing risk.

The Math: When It Makes Sense (and When It Doesn’t)

Using home equity only makes sense when what you earn beats what you pay to borrow.

ROI on borrowed equity > after-tax interest cost

For example, if your HELOC costs 6% and you’re earning 7% from a rental property, you’re ahead. But if the return drops below your loan rate, you’re losing money.

A good rule of thumb is to keep your total loan-to-value under 80–85%. That gives you a safety buffer if home prices fall or rates rise.

If you want a deeper look at what happens when borrowing pushes past that safety zone, my guide on home equity walks through the most common ways homeowners lose money without realizing it.

The Risks Most Homeowners Ignore

Building wealth safely means knowing the downside before it hits.

Rising interest rates can make HELOC payments jump fast, shrinking your cash flow. Falling home values can wipe out your equity cushion and limit your options to refinance or sell.

Overspending is another trap—using equity for cars or vacations turns an asset into long-term debt. And if your income drops or you lose your job, those new payments don’t stop.

Keep a safety buffer and an emergency fund before borrowing. That’s how you protect your home while letting your equity work for you.

How to Protect Yourself While Leveraging Equity

Have an emergency fund that covers at least six months of payments before borrowing.

Choose fixed-rate options when you can—steady payments protect you from rate spikes.

Only borrow what you can invest profitably. If the math doesn’t work, skip it.

Keep personal and investment money separate, and if you’re using equity for property or business, consider an LLC or umbrella insurance for extra protection.

Real-World Example: Turning $80K Equity into $400K Net Worth

Let’s say a homeowner named Mark had $80,000 in home equity sitting idle. Instead of letting it collect dust, he pulled it out through a cash-out refinance and used it as a down payment on a small four-unit rental property.

That property brought in $2,800 a month in rent and covered all expenses with roughly $600 in positive cash flow. After three years, the property appreciated by $60,000, and the mortgage balance dropped another $20,000 through regular payments.

Mark then refinanced that rental, pulled out $60,000 of new equity, and used it to buy another property—doubling his cash flow and increasing his net worth again.

Within six years, the original $80K in home equity had turned into nearly $400K in combined equity and appreciation across multiple properties.

That’s the wealth flywheel in action:

pull → invest → cash flow → refinance → repeat.

When done responsibly, home equity doesn’t just sit… it multiplies.

FAQs About Using Home Equity to Build Wealth

It can be—but it’s risky. The market moves fast, and if your returns dip below your borrowing cost, you lose. Most homeowners are safer using equity for assets they can control, like real estate or high-ROI renovations.

Usually not. Under current IRS rules, HELOC interest is only tax-deductible if the funds are used to buy, build, or improve the property that secures the loan. Always confirm with a tax professional before assuming any deduction.

Keep at least 15–20% equity in your home after borrowing. That cushion protects you if values drop and helps you avoid private mortgage insurance (PMI).

Home equity is the portion of your home you truly own—your home’s value minus what you owe. Net worth is the bigger picture: all your assets (home, savings, investments) minus all your debts.

It adds a new account and increases your total debt, which can cause a small dip initially. But making consistent, on-time payments can help your credit recover and even improve over time.

Let Your Equity Work Harder Than You Do

Most people spend 30 years paying off their home. The wealthy figure out how to make their home pay them back in less than 10.

The difference isn’t luck, it’s strategy. They know how to use equity as a tool, not a crutch. They borrow with purpose, invest with discipline, and always understand the math before they move.

Your home is more than a place to live, it’s a wealth-building engine. Use it wisely, and it can create freedom long before the mortgage is gone.